Brown-Forman's FY2024

Jack Daniel's hits an air pocket

I’d like to share a yearly update to my review of Brown-Forman’s 15 year performance history with some notes from the company’s Q4 FY2024 results.

Q4

Three factors seem to have played key roles in determining the company’s operational profitability:

Brown-Forman’s depletion volumes hit their 3 year lows.

At the same time, company’s pricing seems have reached a local peak on USD basis.

Brown-Forman has been investing in its own distribution networks in various large and small international markets. The idea is that the company will be able to improve its reach to retailers as well as consumers much further than a 3rd party distributor would be incentivized to. Japan and Italy are two major markets where Brown-Forman is in-sourcing its distribution network. However, this move also is also bringing initial setup costs as well as permanently higher expenses from running a bigger organization. Consequently, SG&A expenses reflect this change.

The outcome of these factors has been disappointing profits from operations.

FY2024

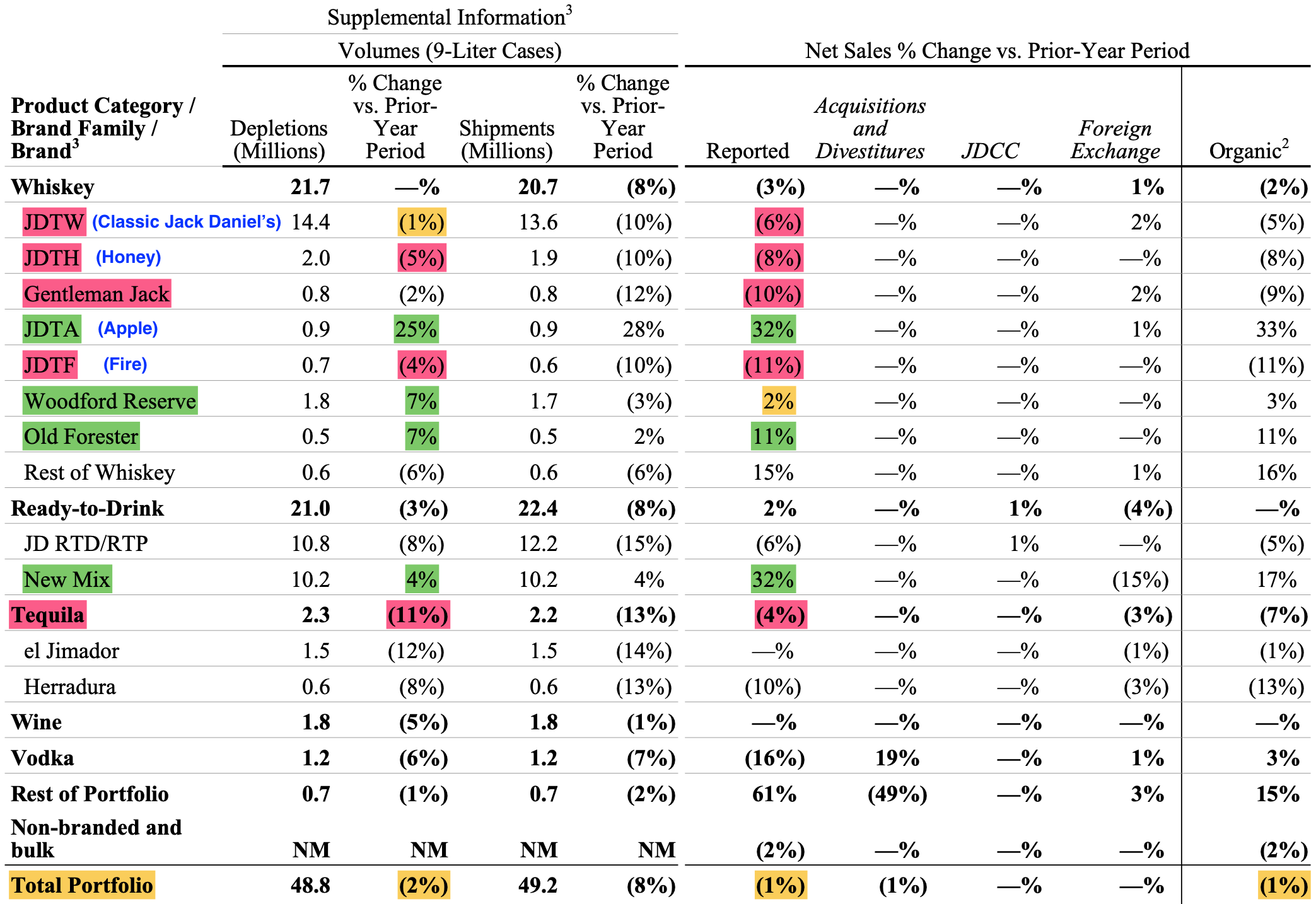

On an annual perspective, Brown-Forman’s all four main product categories lost volume compared to the previous year.

In the last 5 years (from FY19 to FY24), company’s net sales grew by more than 25%, but its operational “core” profits grew less than 4%.

Company’s operational profitability hit 15 year lows this year. One would need to go back to FY2009 to find lower operational margins.

Earnings

One good news — at least on paper — have been the record high EPS of $2.14. However, it is important to note that this number includes Brown-Forman’s sale of its vodka and wine businesses in the year. One-off gains from those dispositions made up close to 20% of the EBIT. In a simplistic view, EPS from business operations could be taken closer to $1.75.

Products and Markets

During the past financial year, one can point to the following product categories and markets as the highlights and the low-lights in generating growth.

Product low-lights: Jack Daniel’s (including the Honey and Fire flavors as well as the Gentleman Jack premiumization) & Tequila brands

Product highlights: Jack Daniel’s Apple, Woodford Reserve, Old Forester, New Mix Tequila RTD

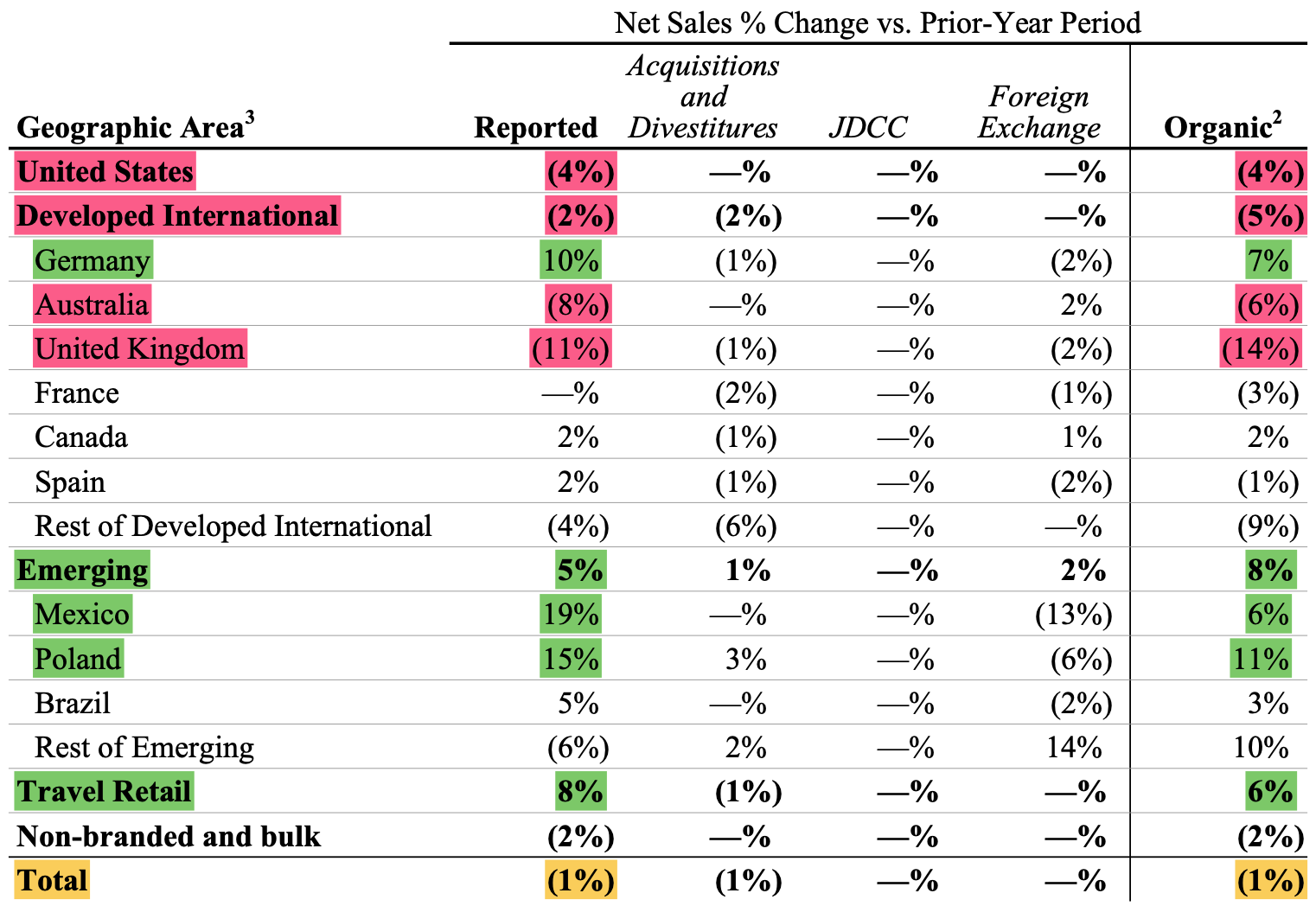

Market low-lights: USA, Australia & UK

Market highlights: Germany, Emerging Markets, Travel Retail

It’s not hard to see that the recent declines have hit Brown-Forman’s three most critical segments of USA as well as the Jack Daniel’s and the tequila brands.

Management foresight & execution

Management’s growth outlook for FY24 has been reduced step-by-step every quarter during the year.

Outlook for the organic sales growth started the year at 6% and was reduced to 0% by Q3. Nevertheless, the company even missed this target and ended the year at -1%.

Outlook for the organic operating income growth started at 7% and was eventually reduced to 1%. Company missed this target as well and ended the year with -2%.

My conclusion from this recent track record is that Brown-Forman’s business is going through a (hopefully temporary) upheaval which the management calls “normalization” and doesn’t seem to be able to forecast into the near future accurately. Hence, in my opinion, the FY25 growth outlook of +3% is not yet a reliable target.

Disclaimer: This is not investment advice. Please read the full disclaimer in the About page.