15 Years of Brown-Forman

A "medium-term" look into a deeply long-term company

Brown-Forman is the 153 year old family-controlled spirits producer, most famous for its Jack Daniel’s family of Tennessee whiskeys. I would highly recommend Price to Wealth’s excellent write-up of the company from two years ago as an introduction to the company’s history and strategy.

In the past 15 years that included GFC, COVID-19 and the Russian War, Brown-Forman grew volumes at a CAGR of 2.1%. Over that period, the company increased its concentration in premium and ultra-premium whiskey and tequila brands while exiting various wine, vodka and lower-tier spirits brands.

Today, over 90% of the company’s volume consists of whiskeys and tequilas, along with their Ready-to-Drink variants. Management expects their newly acquired ultra-premium gin and rum brands to lead the growth for the rest of the portfolio.

In the same time frame, sales and operating profits compounded at around 3.9%.

Brown-Forman’s costs and expenses as a percentage of sales show drastically different dynamics in the first and second half of these 15 years.

In the last 7 years, share of costs of goods sold rose sharply due to increases in raw material costs and supply chain disruptions. Brown-Forman’s pricing strategy of periodic yet nominally low rates of hikes (arguably somewhat similar to the pricing policy of Hermès) in contrast to competitors suggests that it might take a while for the gross margins to recover despite their brands’ available pricing power.

On the other hand, management has managed to reduce the SG&A margins with their discipline and operating leverage while keeping interest expenses in check thanks to a conservative balance sheet. One aspect that slightly concerns me despite its positive financial effect is the decreasing share of advertising expenses. With many viable avenues for growth in RTDs and ultra-premium spirits, increased advertising seems like a critical investment for Brown-Forman’s future hits.

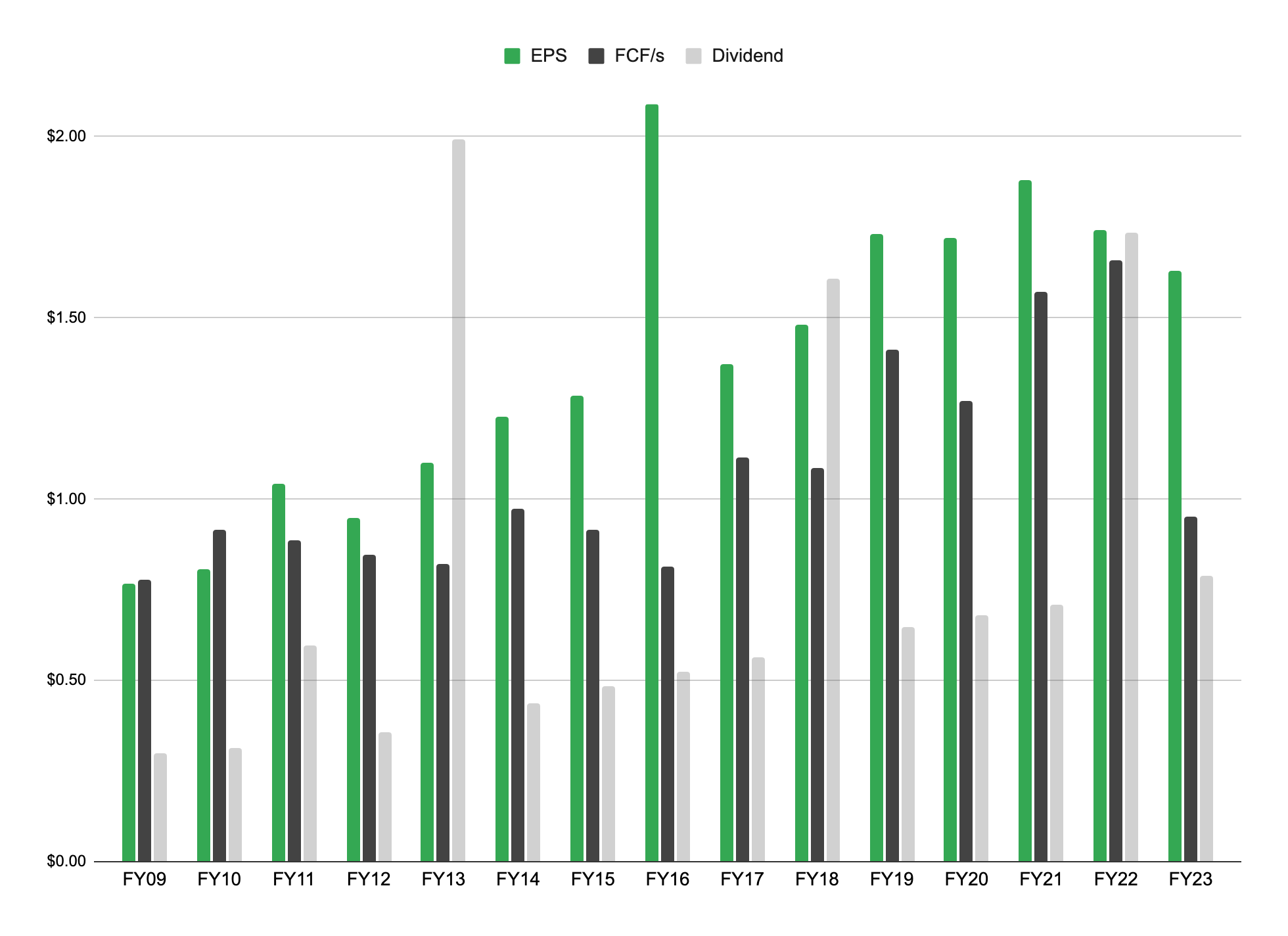

Finally, we can look at the results from a shareholder’s perspective.

Disclaimer: This is not investment advice. Please read the full disclaimer in the About page.