Philip Morris: An Owner's Review

PMI in a few charts

Thesis

My thesis in owning Philip Morris International has been very simple over the last 7 years: PMI has the culture and the products to sustainably grow its recurring profits for the long-term.

Business Review

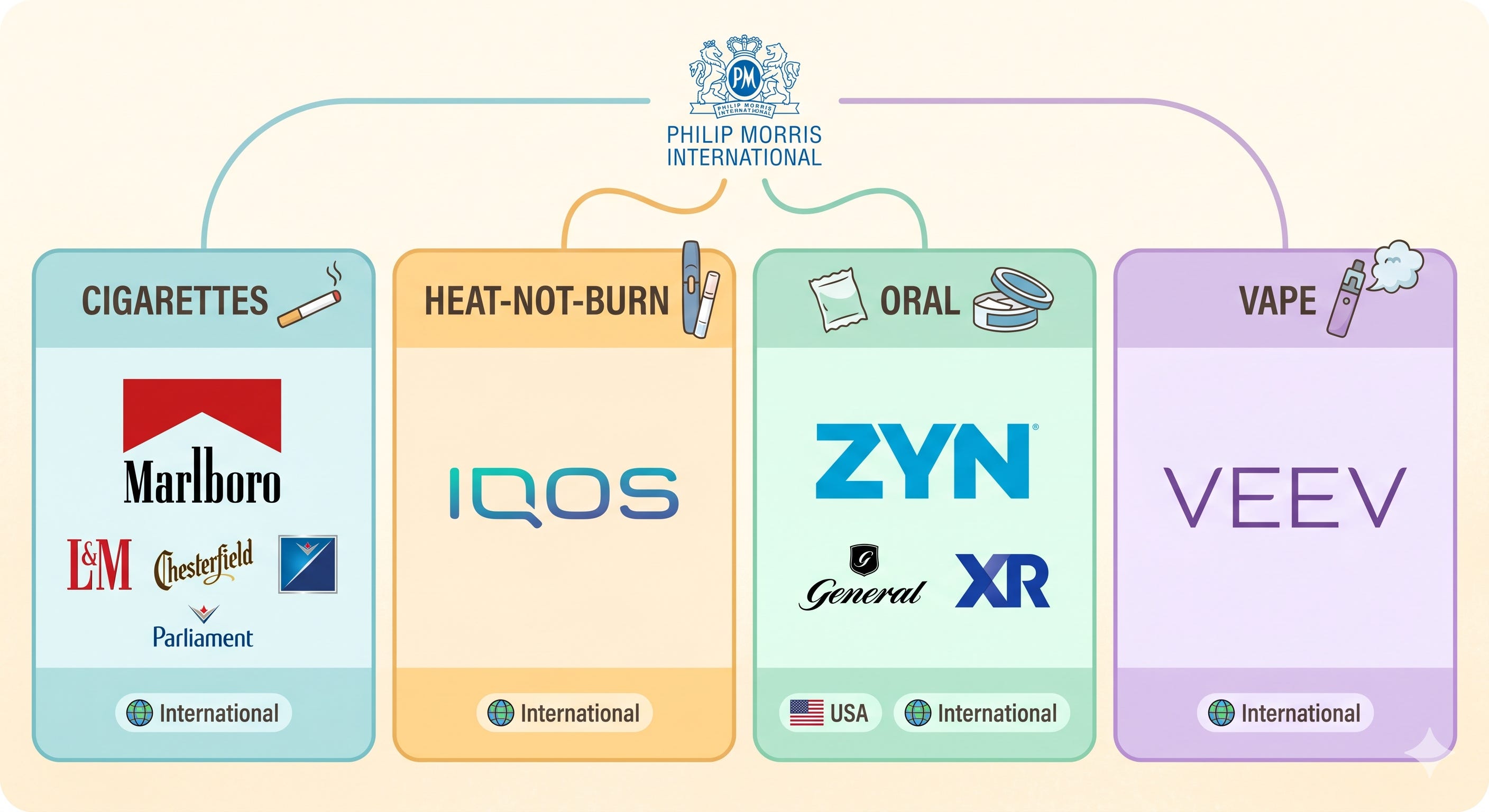

Philip Morris International has three primary lines of sales:

Cigarettes outside the USA and China

Smoke-free nicotine products (heat-not-burn, vape and oral) outside the USA and China

Smoke-free nicotine products in the USA1

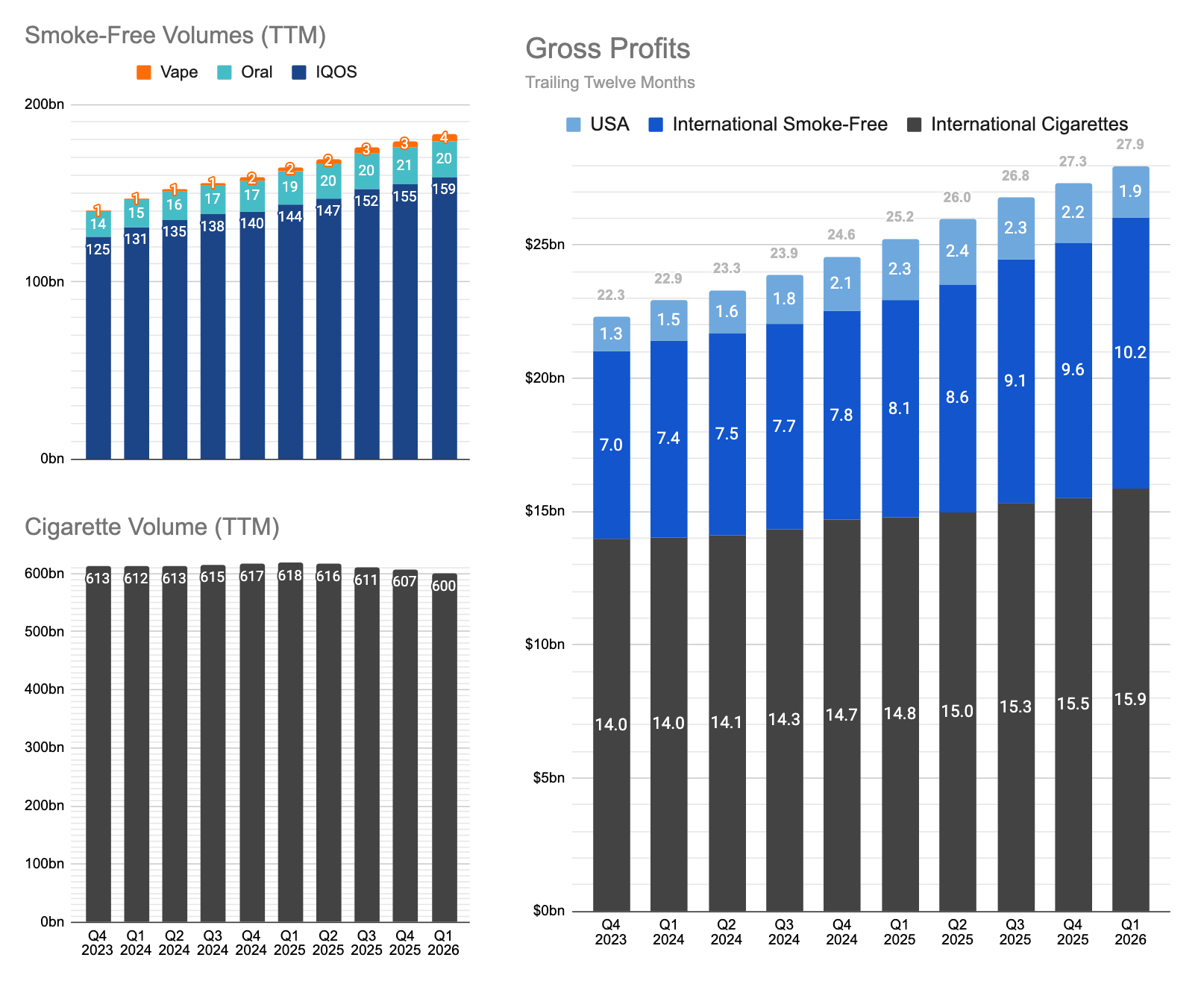

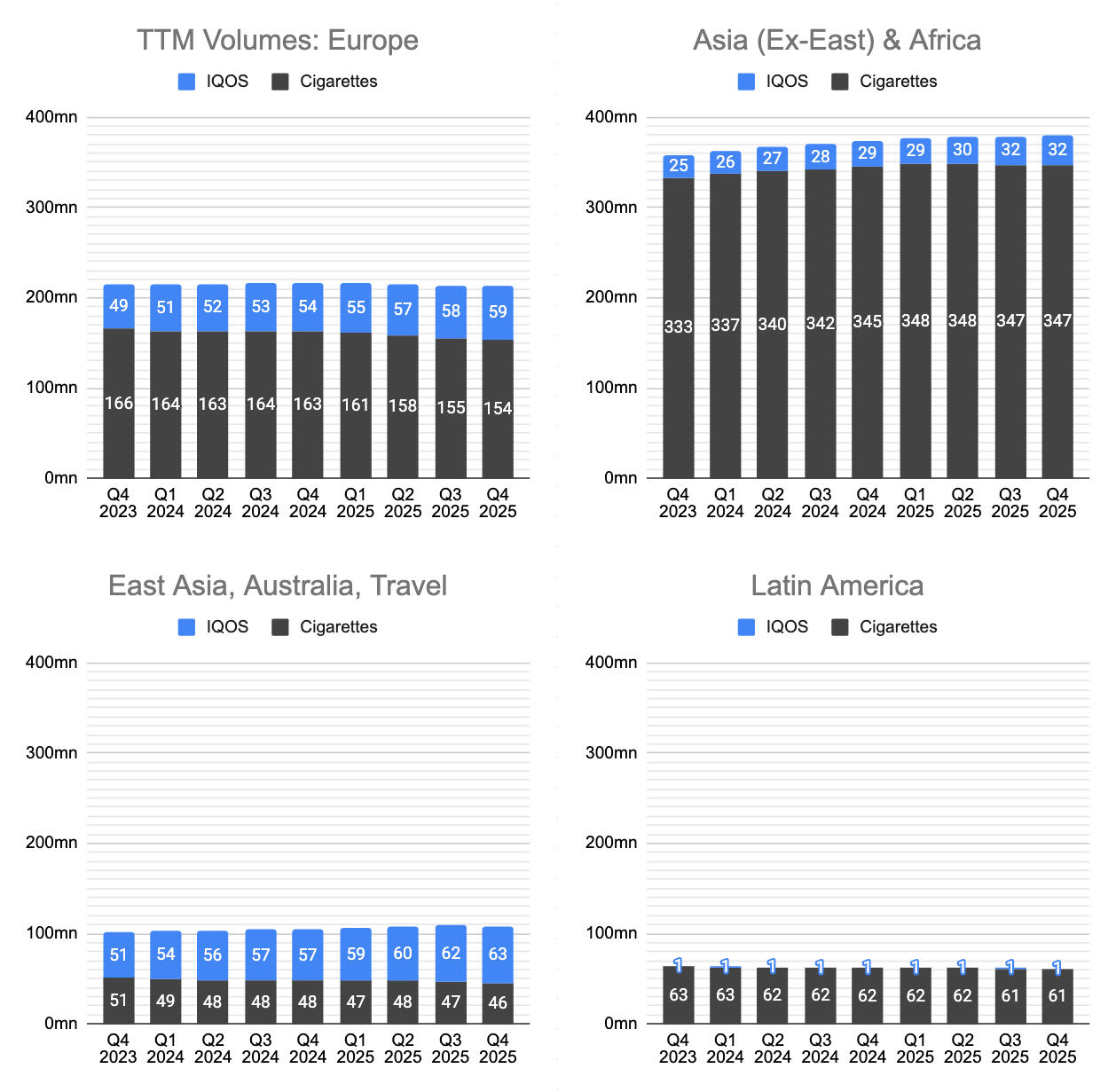

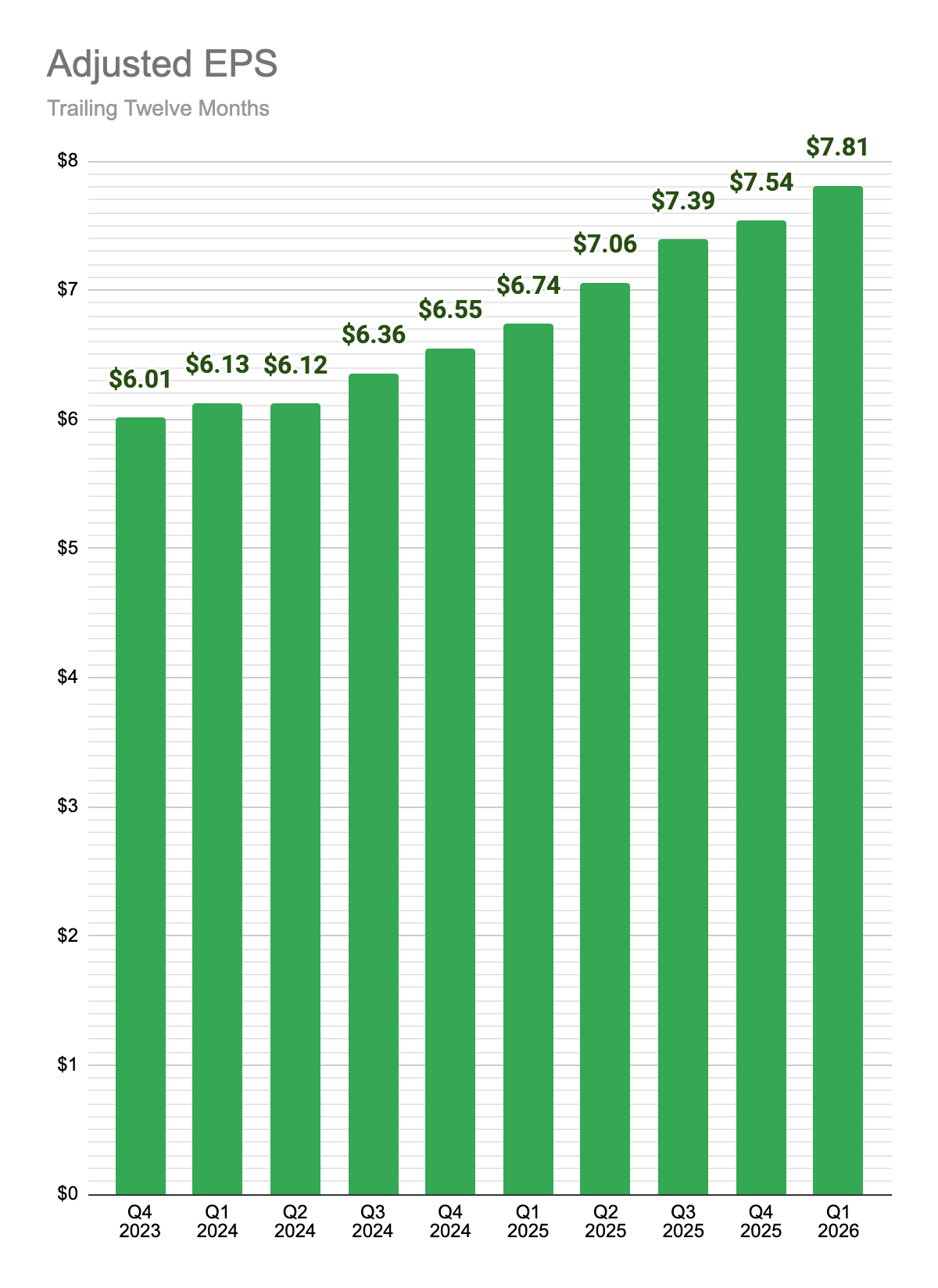

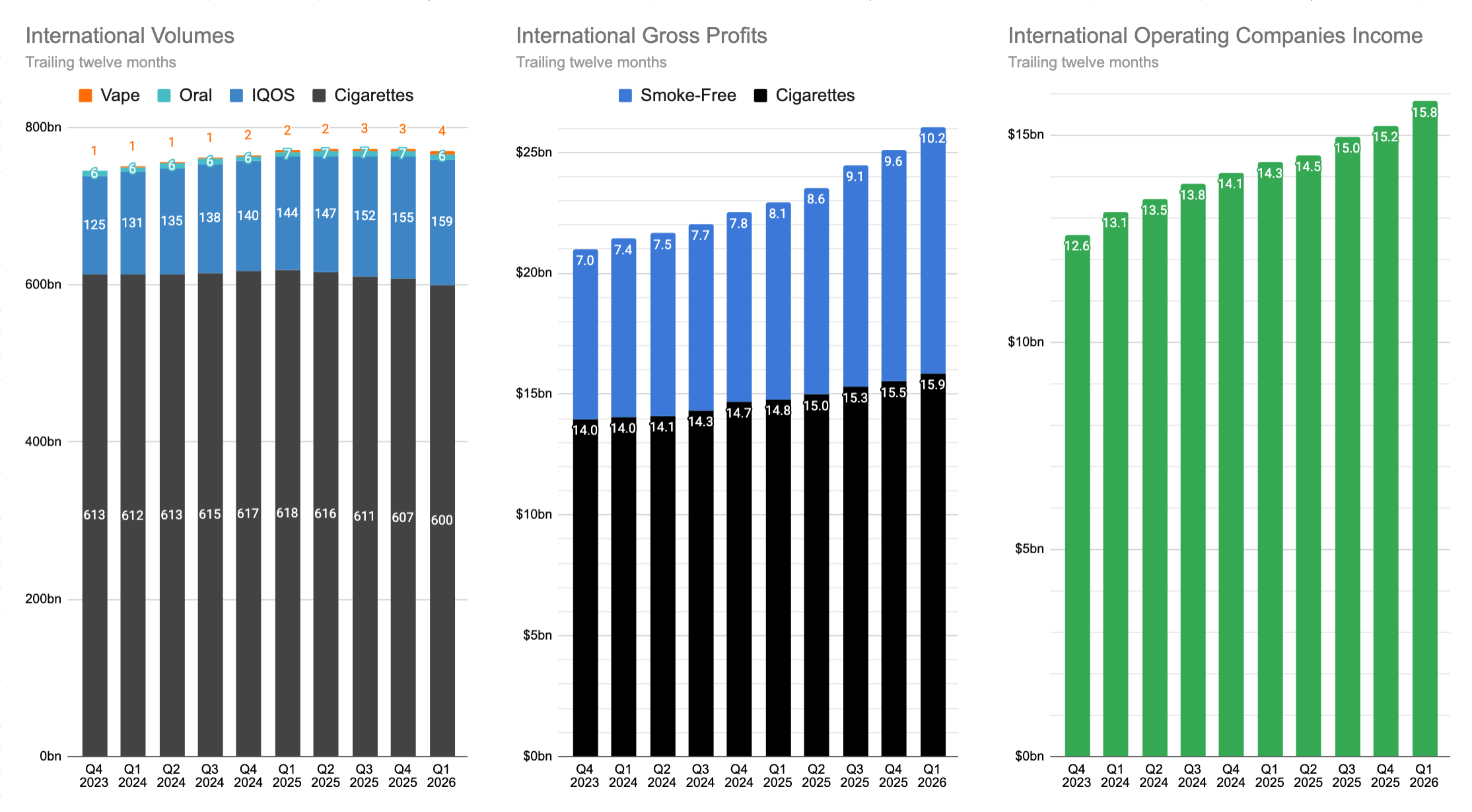

Below is the the main dashboard I use to track PMI’s operational performance.

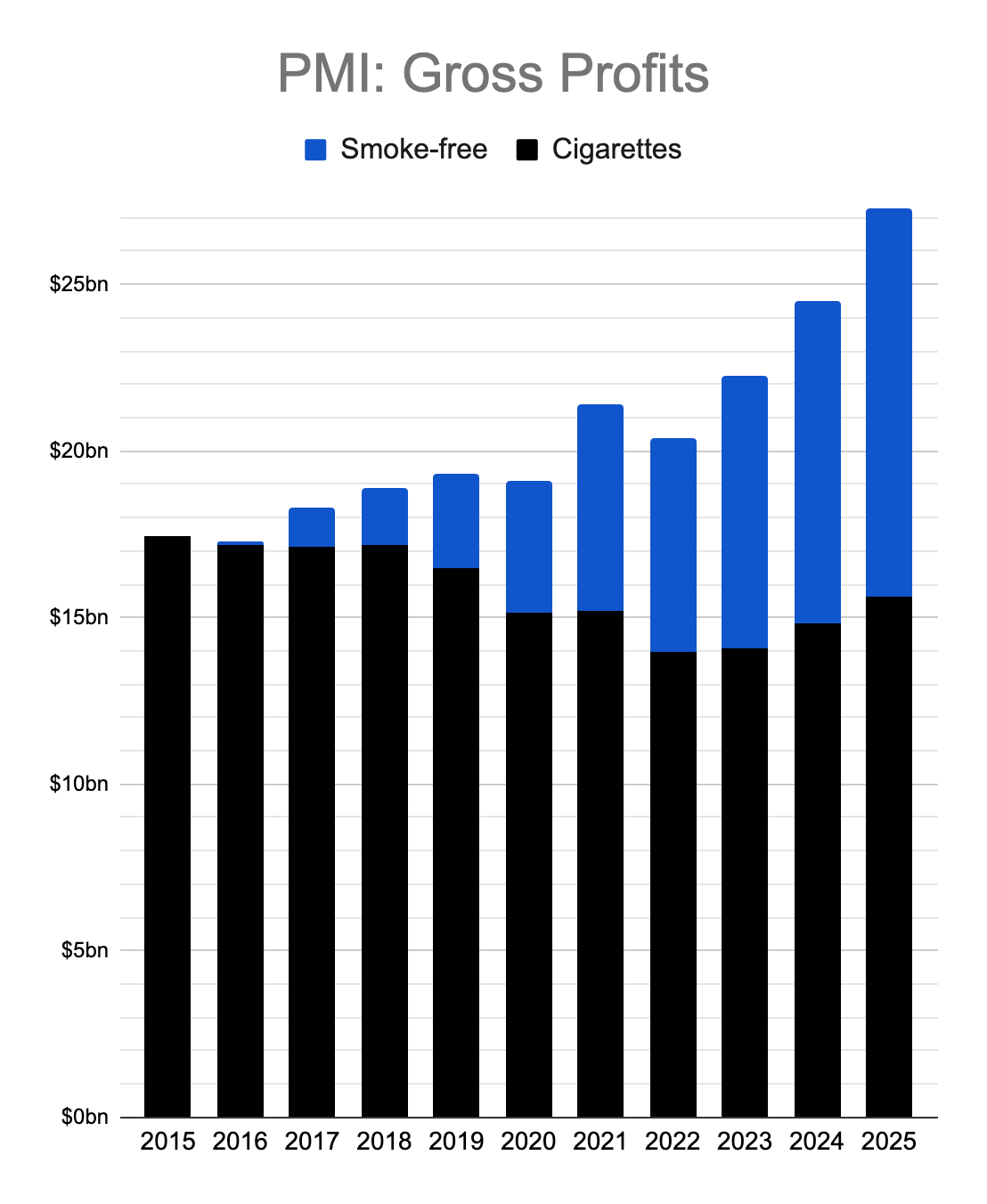

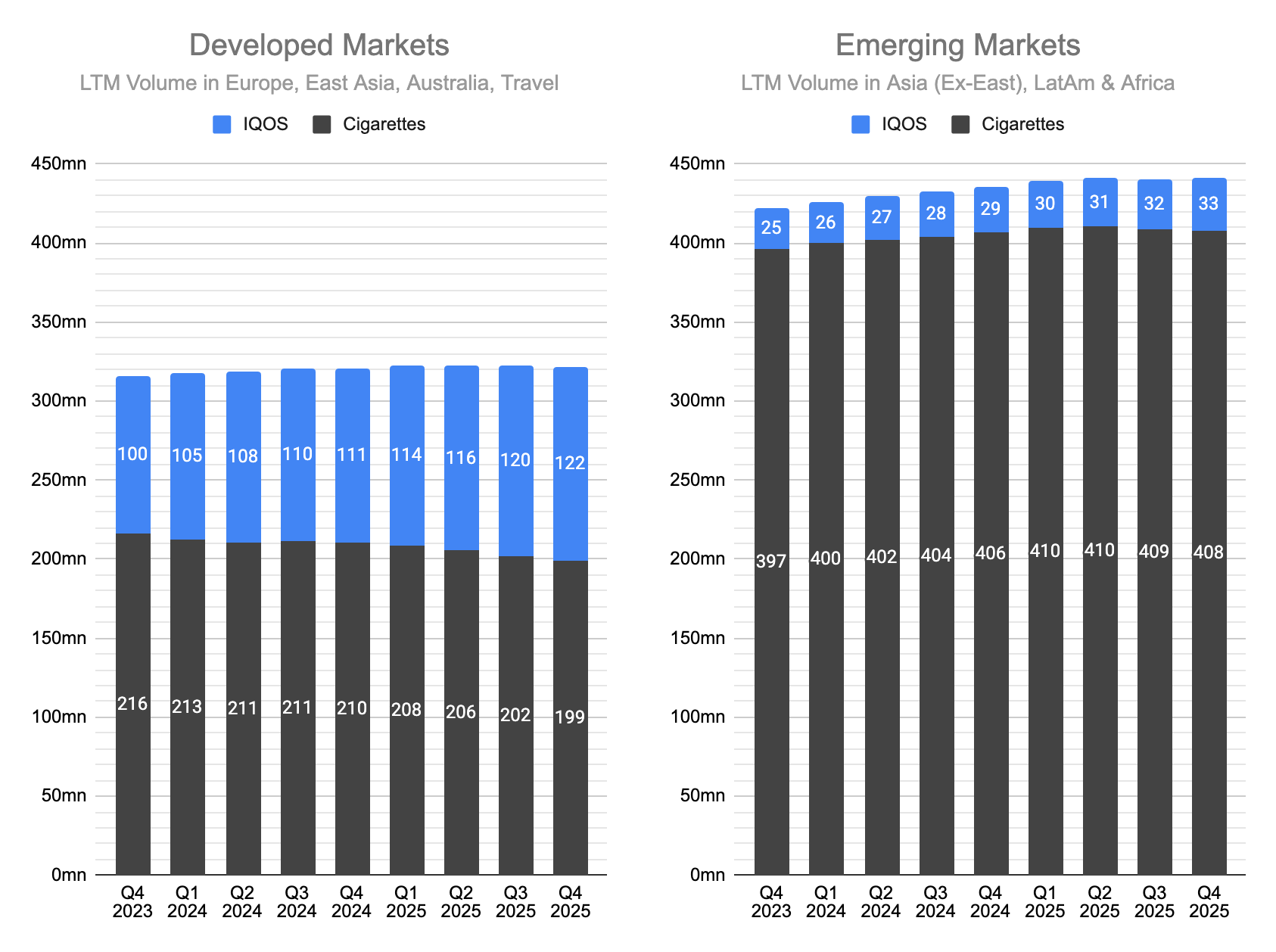

We can already see that the company’s profits largely depend on two products: Cigarettes and IQOS. PMI manages to squeeze steadily increasing profits from slowly declining cigarette volumes and powers its profit growth on the back of expanding IQOS consumables.

In fact, the much touted entry into the U.S. market (via the Swedish Match acquisition) is not yet contributing to earnings.

So, one could roughly estimate that 2/3rds of PMI’s earnings depend on cigarettes and 1/3rd on IQOS.

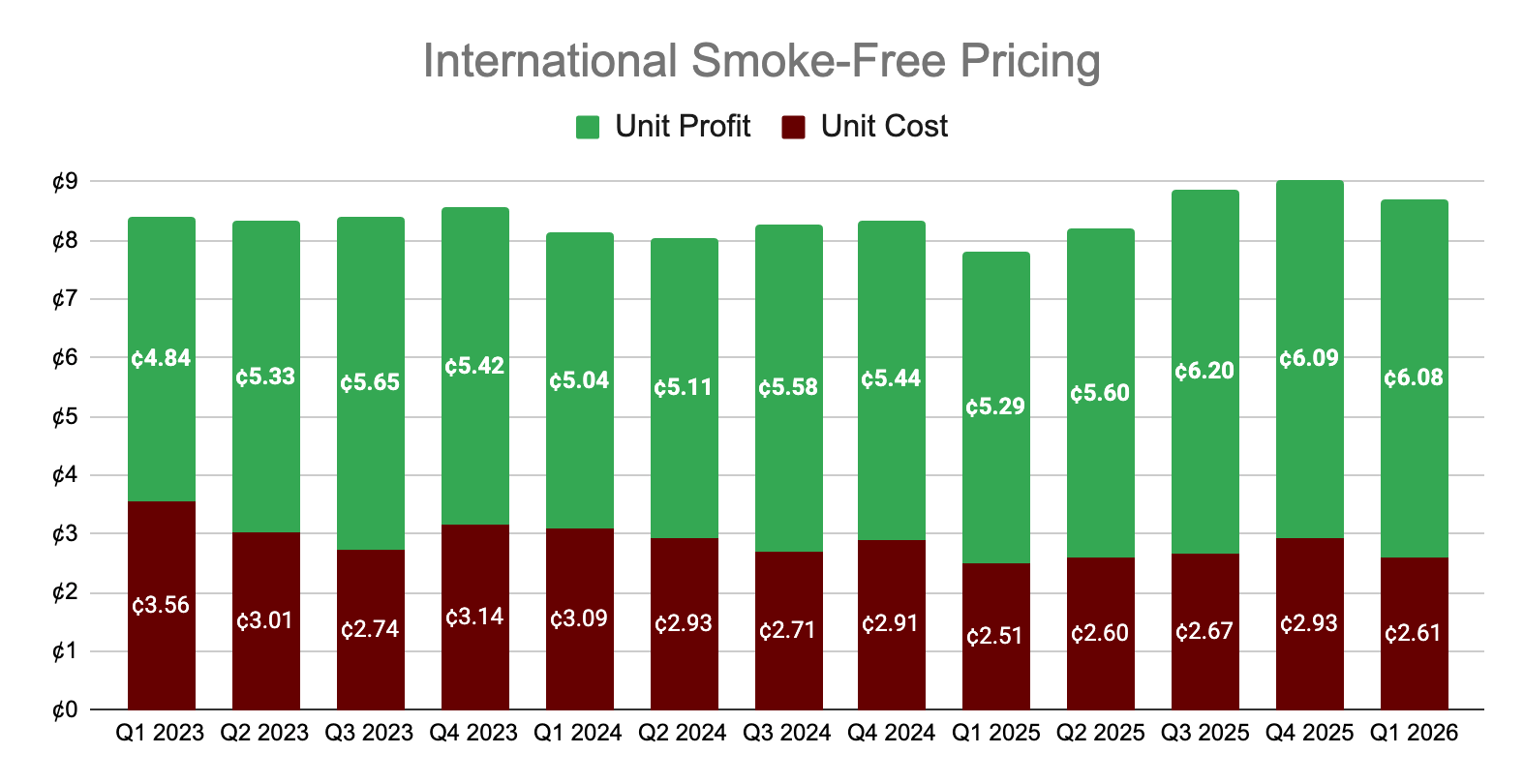

Breadwinners: Cigarettes and IQOS

PMI has managed its smoke-free transition without a significant volume loss in its major markets.

For a category-defining product line that aims for highest regulatory standards and luxury positioning, PMI has rightly prioritized Europe and Japan in its IQOS expansion.

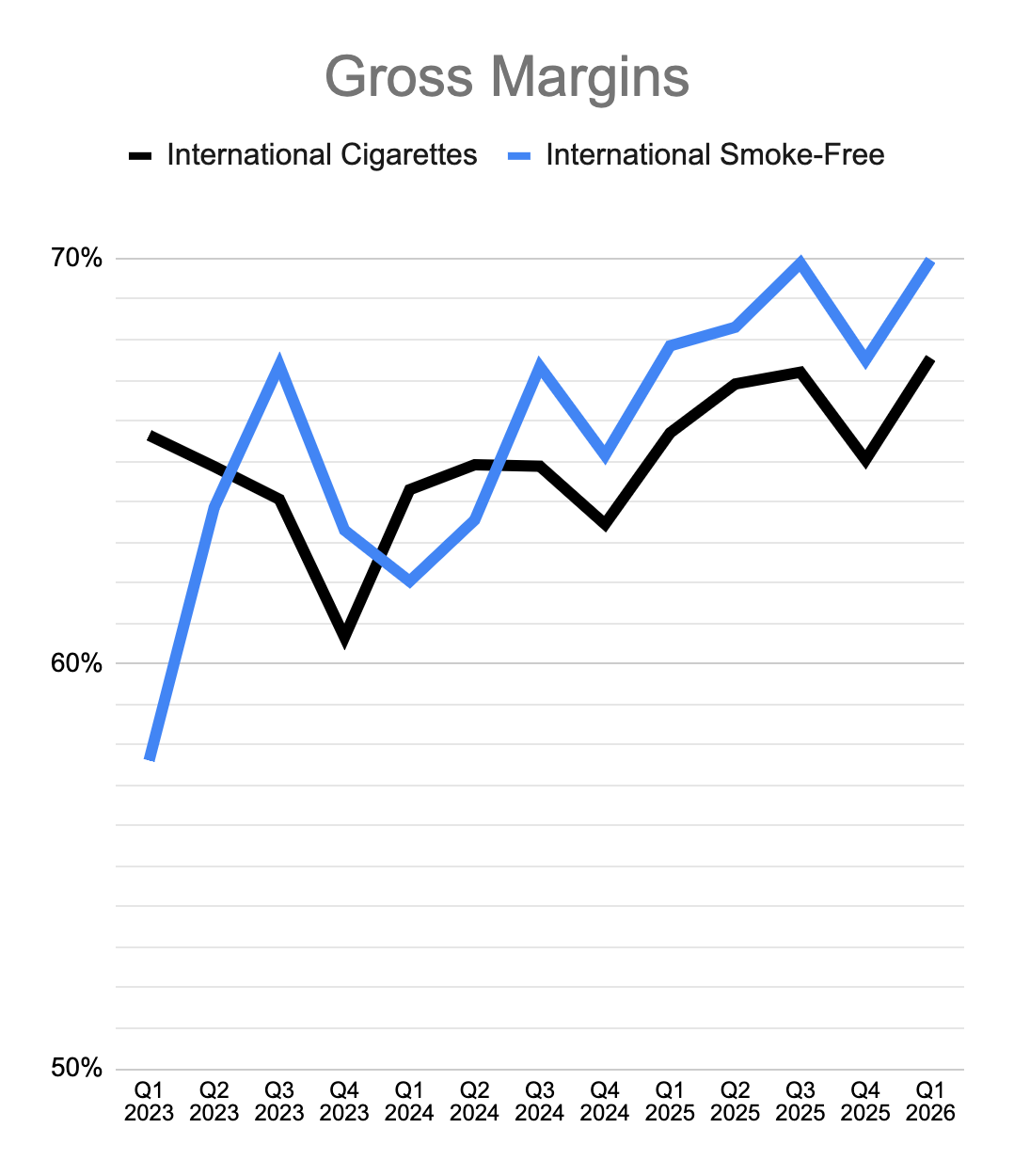

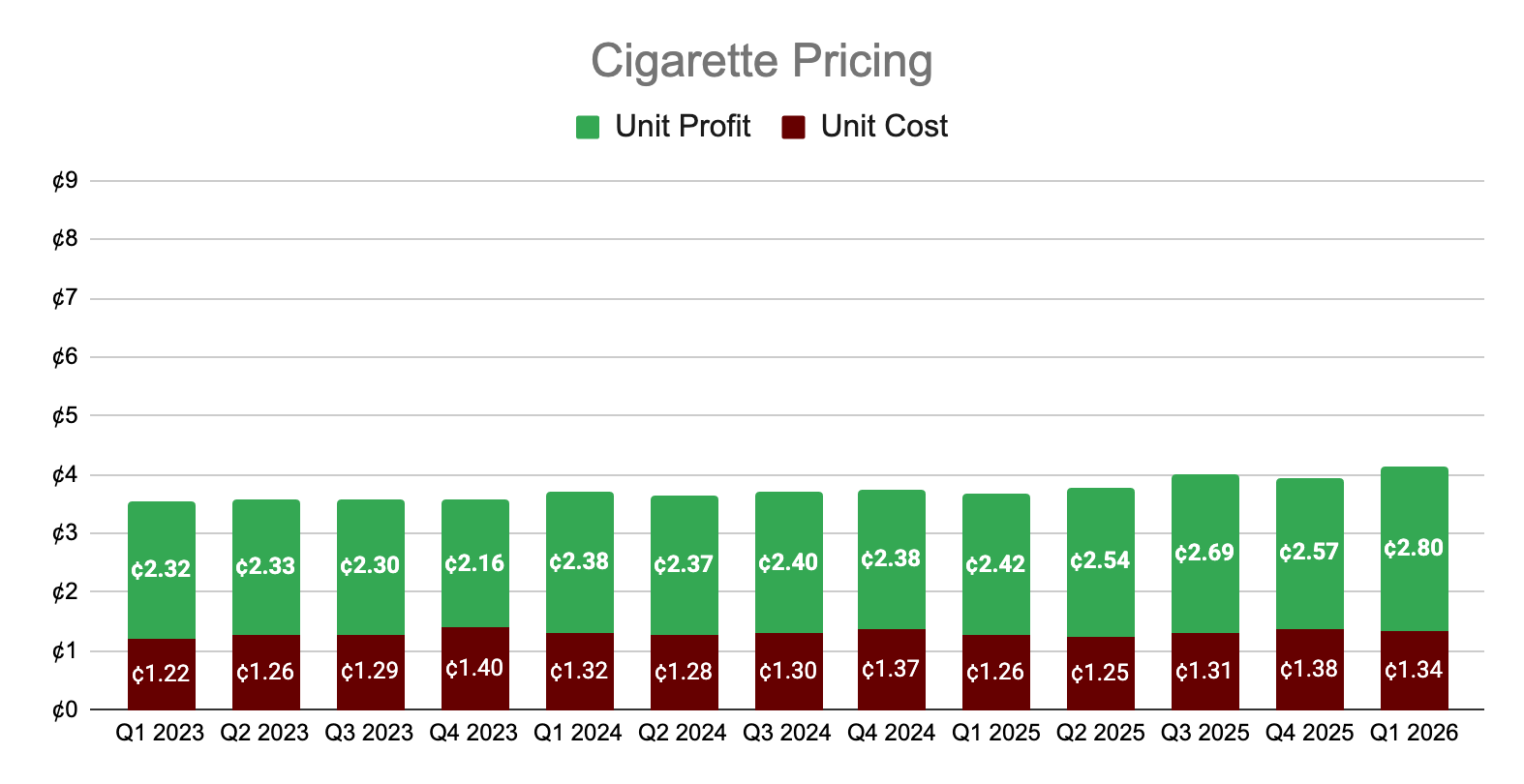

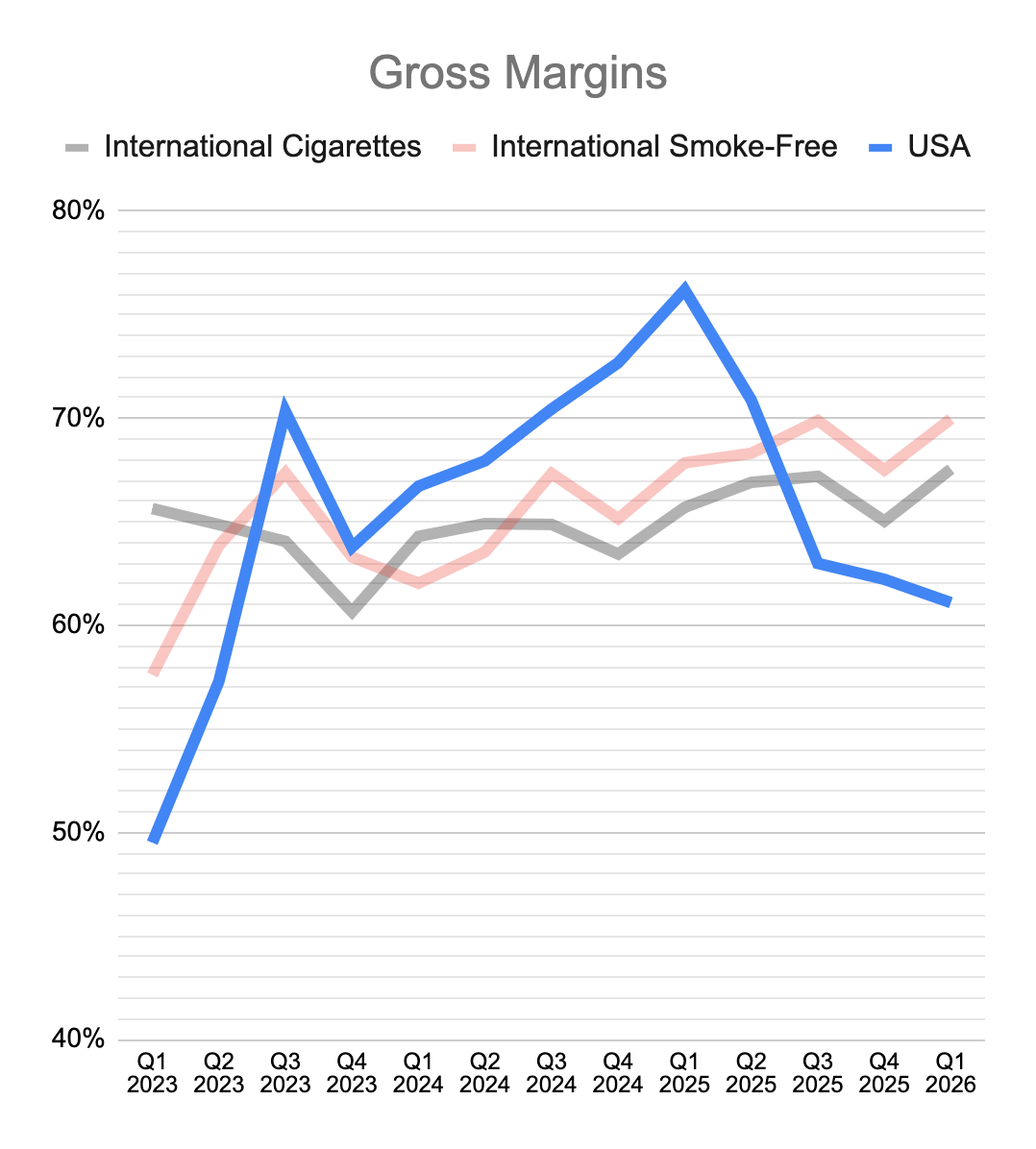

IQOS not only comes with higher margins than the mature cigarette business but also earns more than double gross profit per stick thanks to its pricing power and production efficiencies.

Upside Potential

Regardless its past performance, holding on to any company requires an expectation for its future.

I see three reasons to be enthusiastic about the company’s future.

Upside #1: Same old, same old

Although it may not be very intellectually exciting, PMI’s likeliest source of future profit growth lies in the continuation of its excellent execution of IQOS expansion on top of premium cigarettes in its international markets.

Upside #2: US Smoke-Free

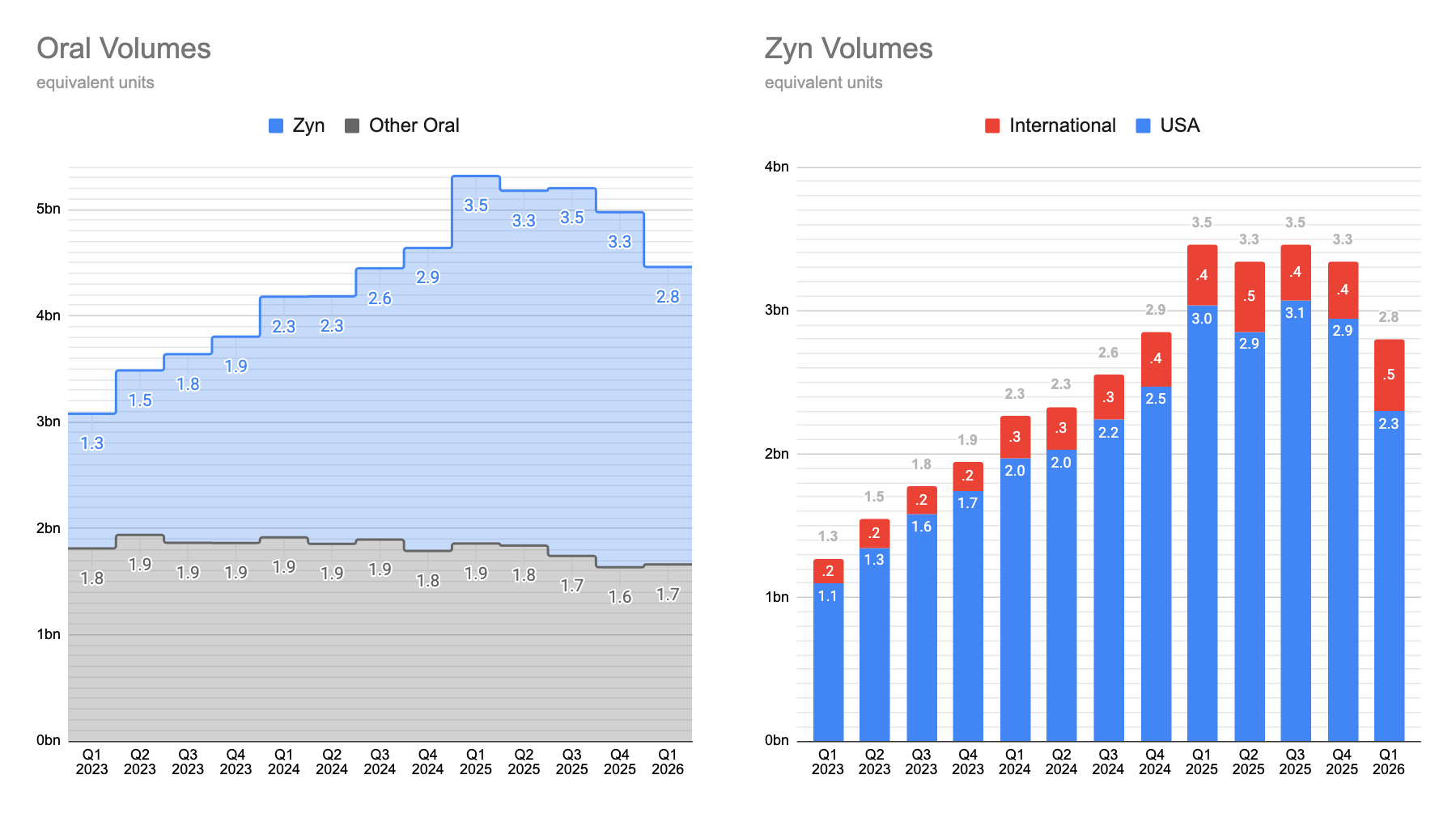

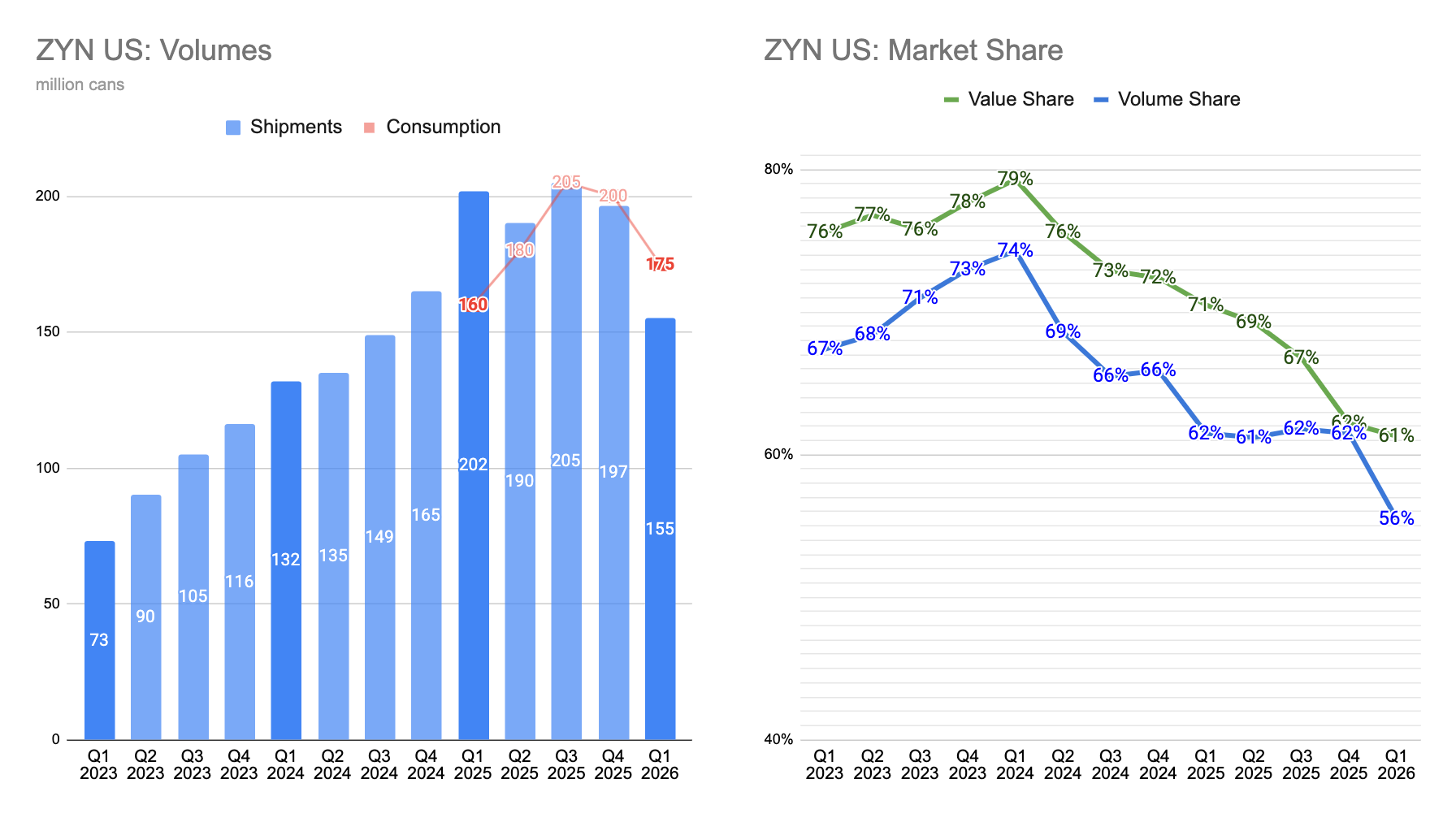

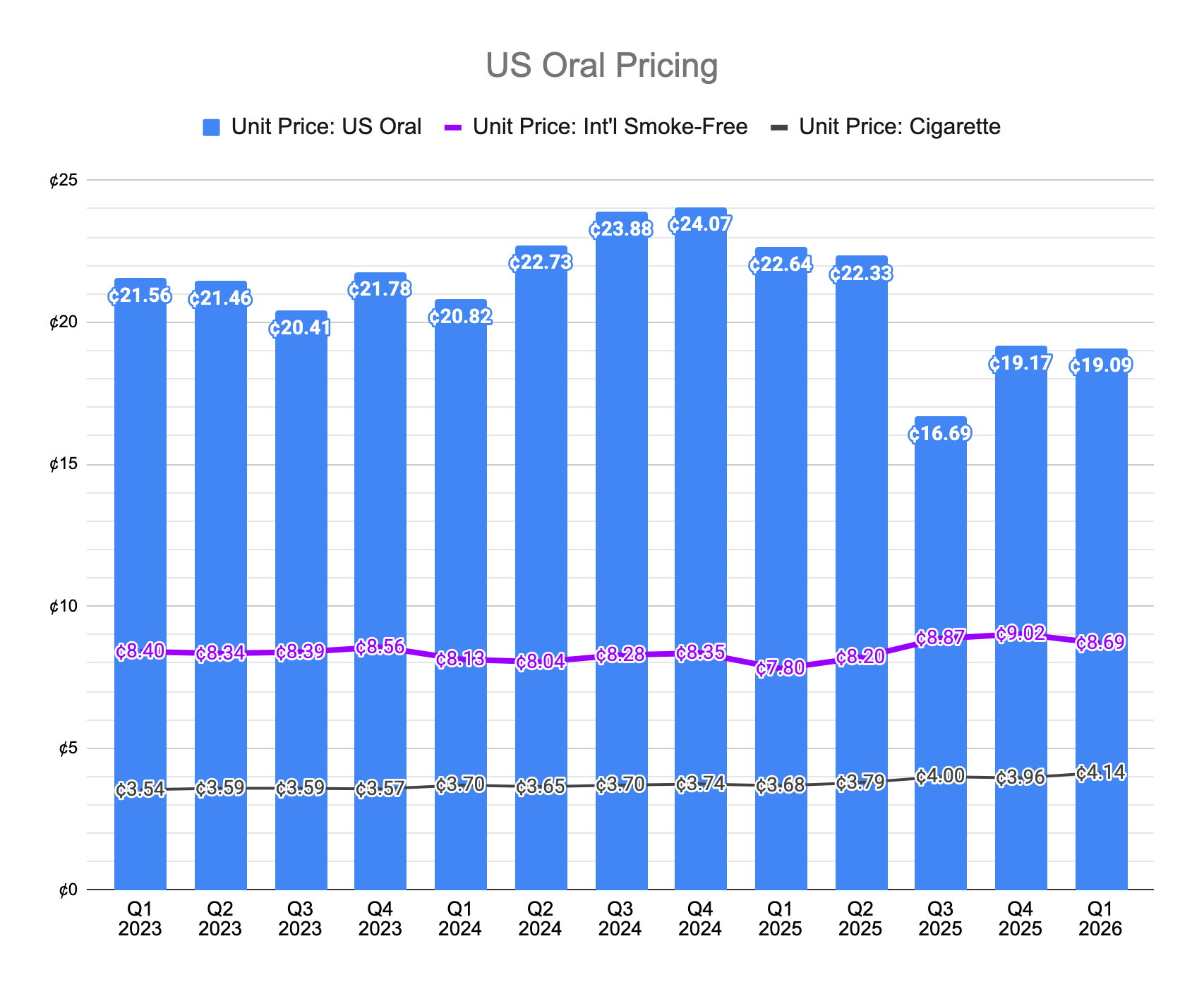

PMI’s newly acquired oral portfolio clearly depends on Zyn sales in the USA for growth.

No matter whether you look at shipments, take-off or market share, Zyn’s incredible growth story seems to have been slowing down lately.

It is not impossible that Zyn reaches its peak consumption in the near future and may even start shrinking in nominal terms against the competition in the ever-changing U.S. smoke-free market. However, if you don’t take that doomsday view, perhaps even at slower growth rates, Zyn provides an interesting upside potential for a couple of reasons.

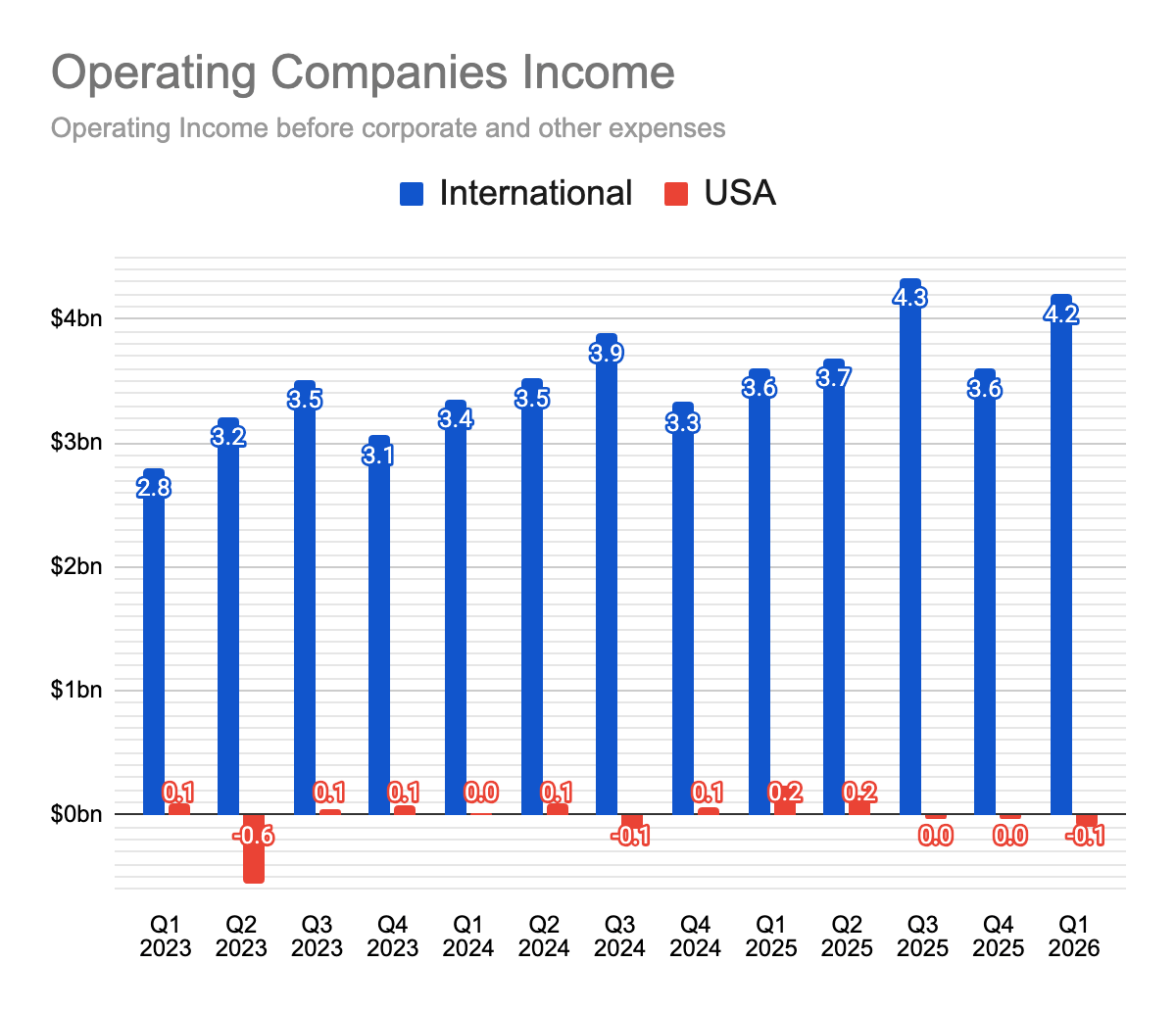

Firstly, Zyn US has contributed no earnings to the company’s bottom line even when it generated almost 10% of all gross profits due to its heavy investment phase. One way (demand growth) or another (oversupply), those investments are bound to have a smaller impact on results. When that happens, Zyn will start contributing purely incremental dollars of net income.

Secondly, even at a moderate success scenario where growth remains and the category proves to be brand-loyal, Zyn continues to have an enormous profit potential due to its extraordinary unit economics.

Upside #2.1: IQOS ILUMA

Although it is understandably less talked about due to both the regulatory or the demand-side uncertainties, IQOS in the US remains a very significant potential that could realistically be EPS-moving in a long-term success scenario.

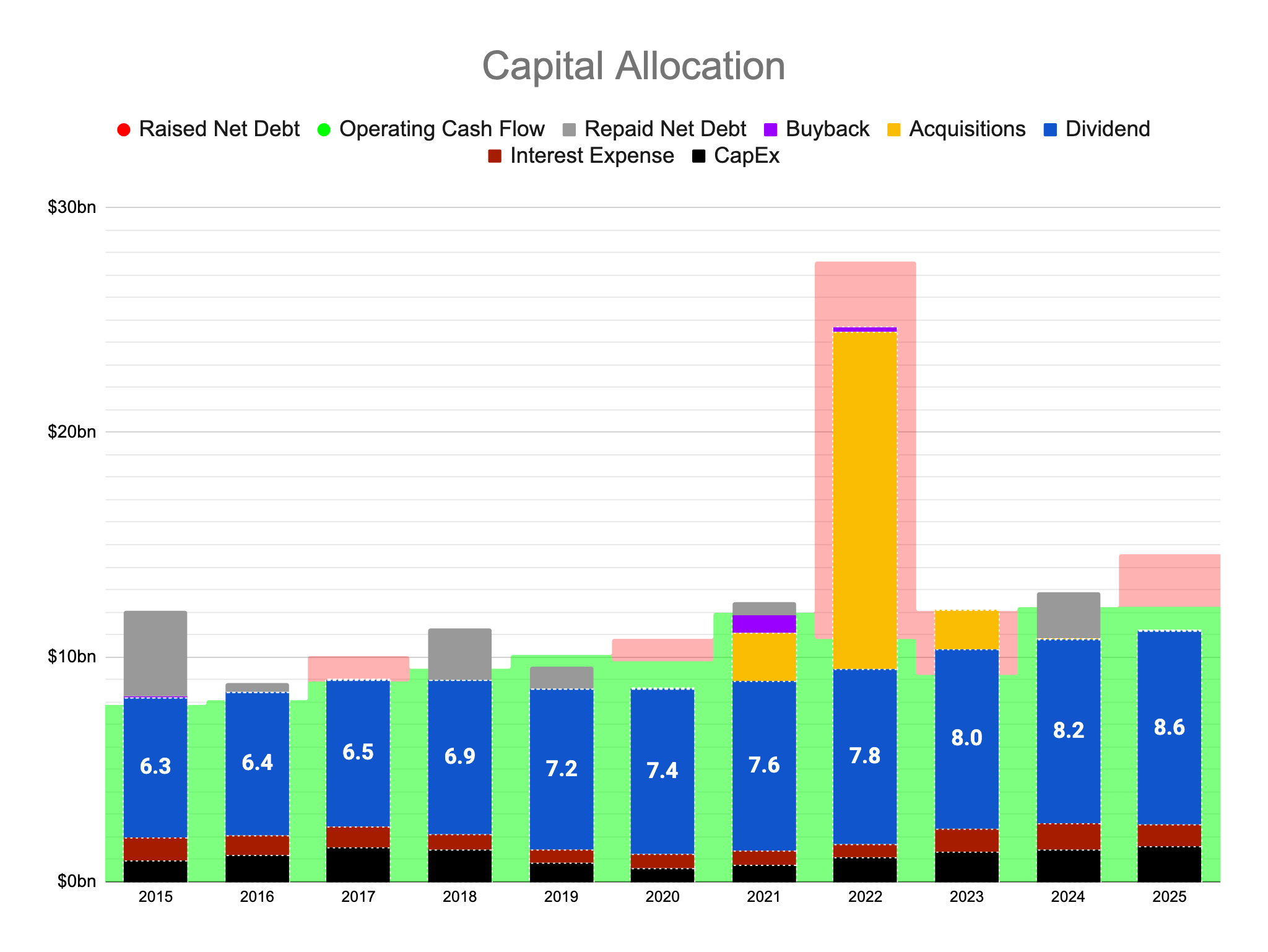

Upside #3: Rational Allocation

Tobacco industry is famous for the way it can delude itself into wasting its gushing cash flows in pointless acquisitions.

In its relatively short 20-year history as an independent company, PMI ended up wasting relatively little shareholder capital in diworsifications. (Namely, PMI spent $2.5 billion for inhalation-delivery pharma companies. These acquisitions largely failed at their goal because inhalation-based dosage turned out to be a hard technical problem and pharmaceuticals developed by a “sin company” foreseeably came with huge PR problems. Compare this to $15 billion which Altria wasted at acquiring vape companies at abysmal returns.)

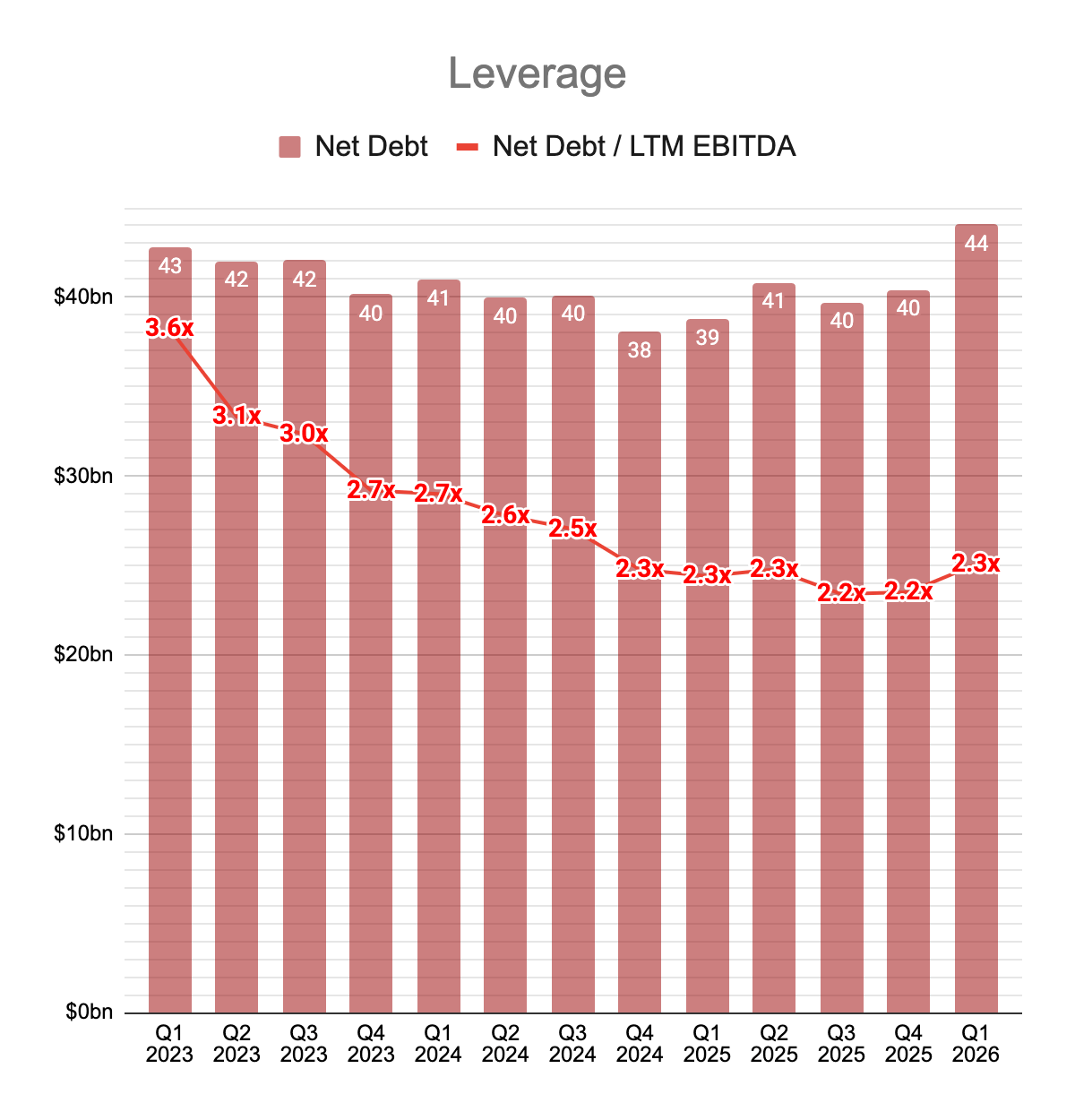

Despite the Zyn-related investment spree in the US, PMI’s post-SWMA leverage is decreasing to the management target of 2x EBITDA , after which the company will have additional cash to allocate.

Although these things can never be truly guessed ahead, I assume that the PMI management will have their hands full with their smoke-free nicotine portfolio both internationally and in the US for many years and will not be looking for non-core or irrational acquisitions.

A growing, nicotine-powered profit flow that is allocated rationally could result in wonderful returns for the long-term shareholder.

Disclaimer: This is not investment advice. Please read the full disclaimer in the About page.

I am ignoring the cigar business inherited from Swedish Match for the sake of simplicity.

Very interesting read Ali.

How do you look at the competitive situation between Zyn and BTI's Velo & Velo+ ?

TV

Thank you so much, Ali, for the great presentation and report 🙏 I really enjoyed it!