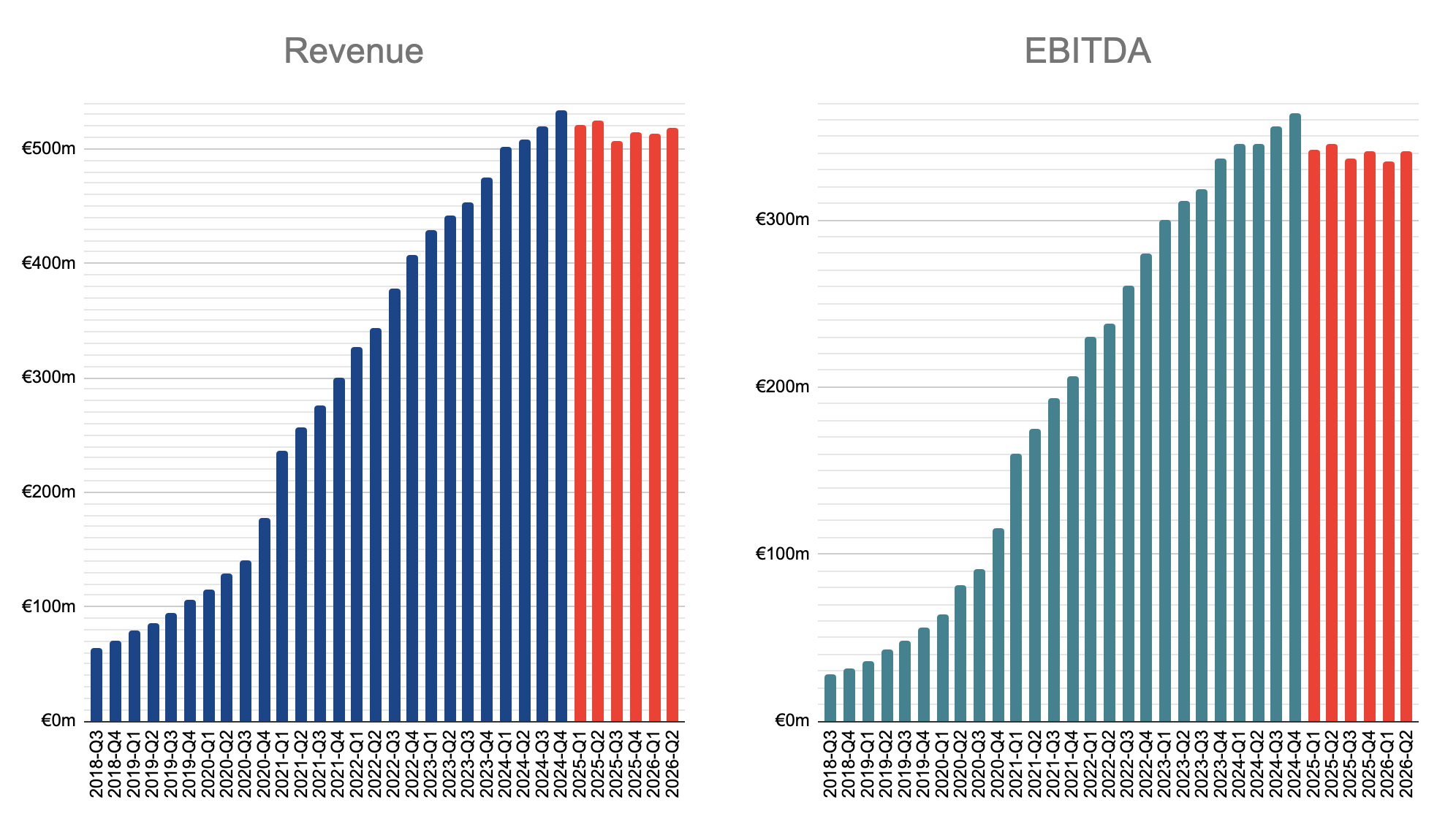

Evolution's Q2 2026

What has happened and what may happen

What has happened:

“I am overall happy with the results in the quarter. Revenue and EBITDA both moved in the right direction” — CEO Carlesund

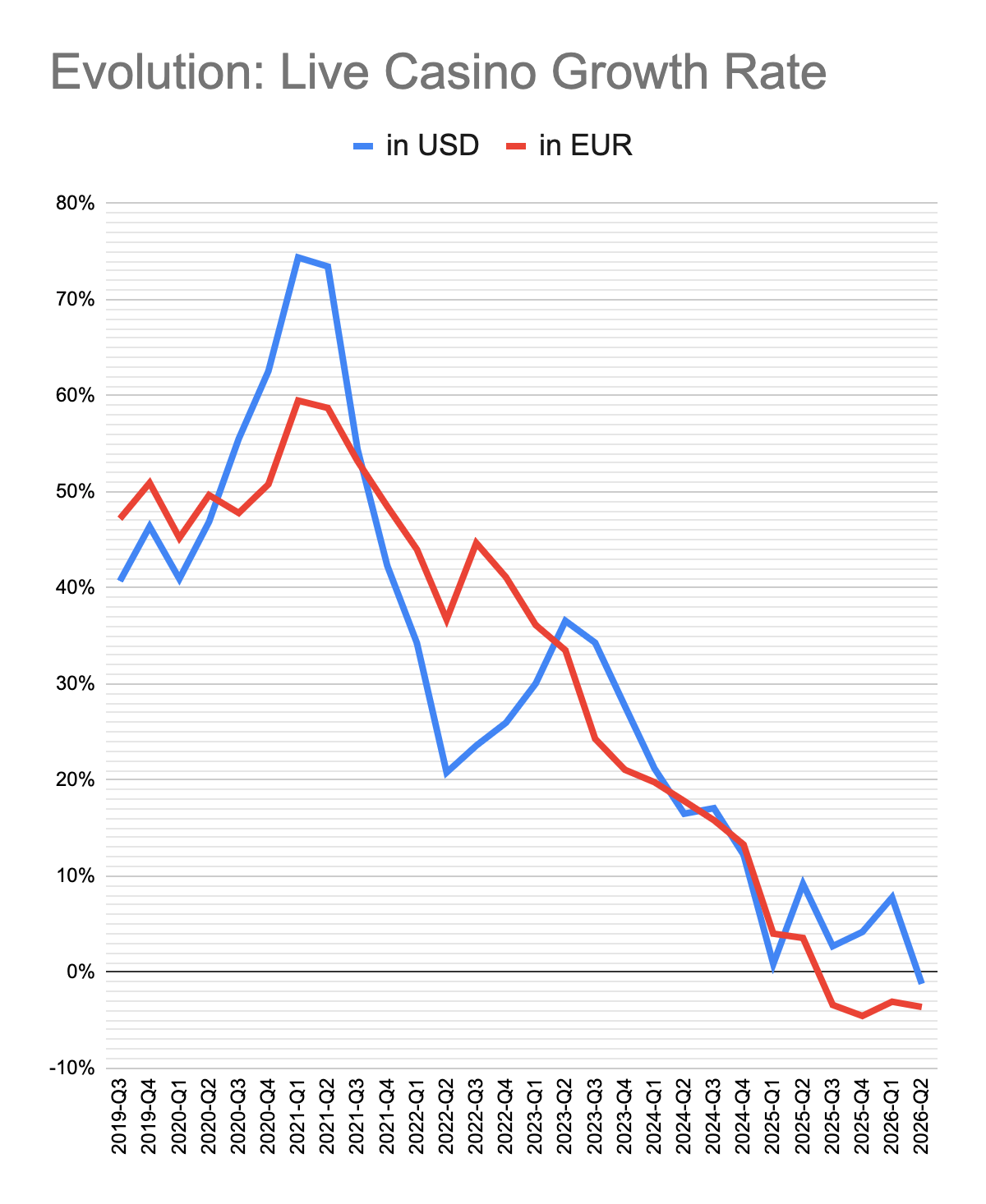

Live Casino

For the first time in its public history, Evolution’s Live Casino declined year-on-year both on EUR and USD bases.

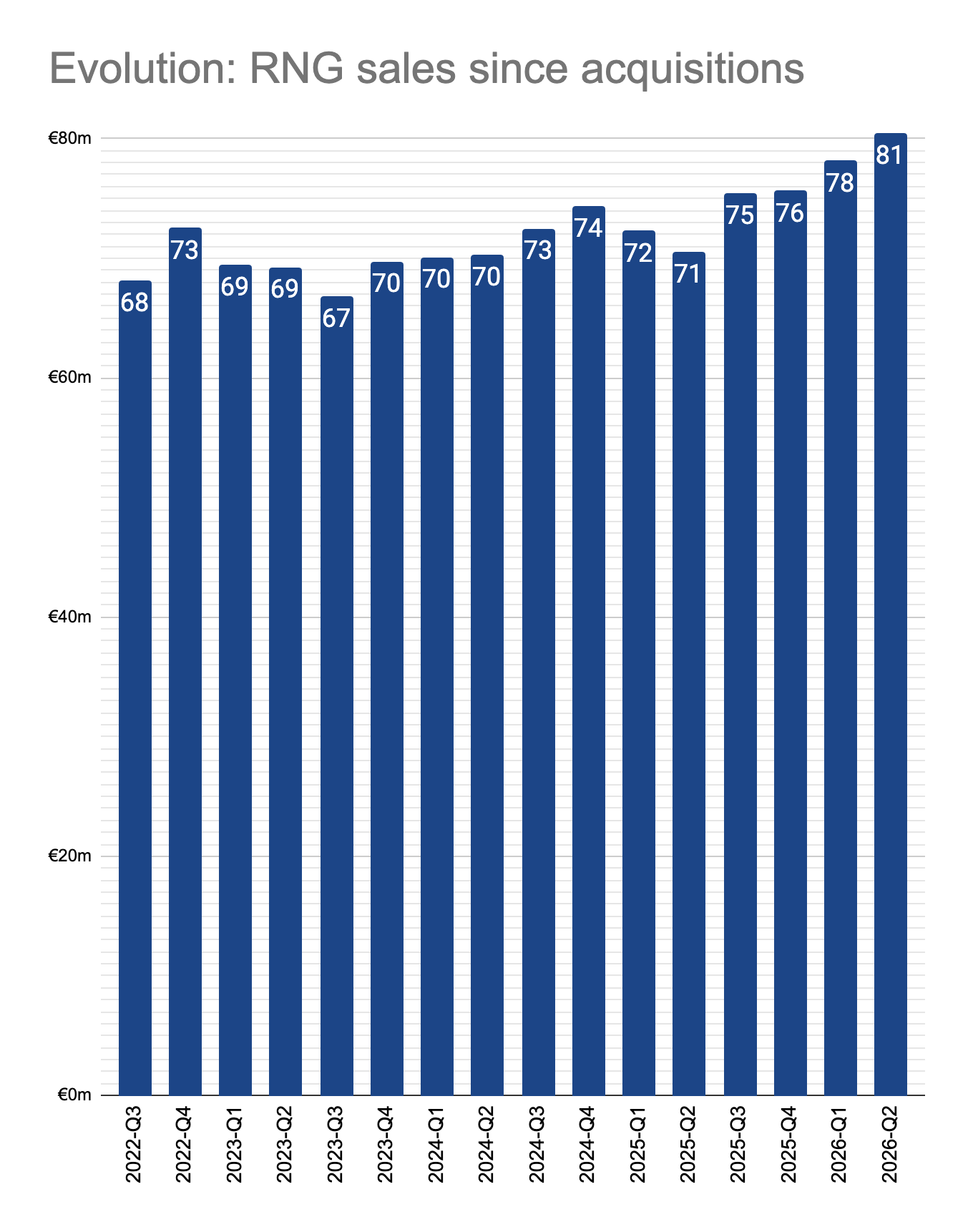

RNG

After 5 years and €2.7 billion, Evolution seems to have finally started its organic growth journey in RNG that makes up 15% of its sales.

“It took a while, but we are here now. And we are proud of that because we stated that we are going to do that.” — CEO Carlesund

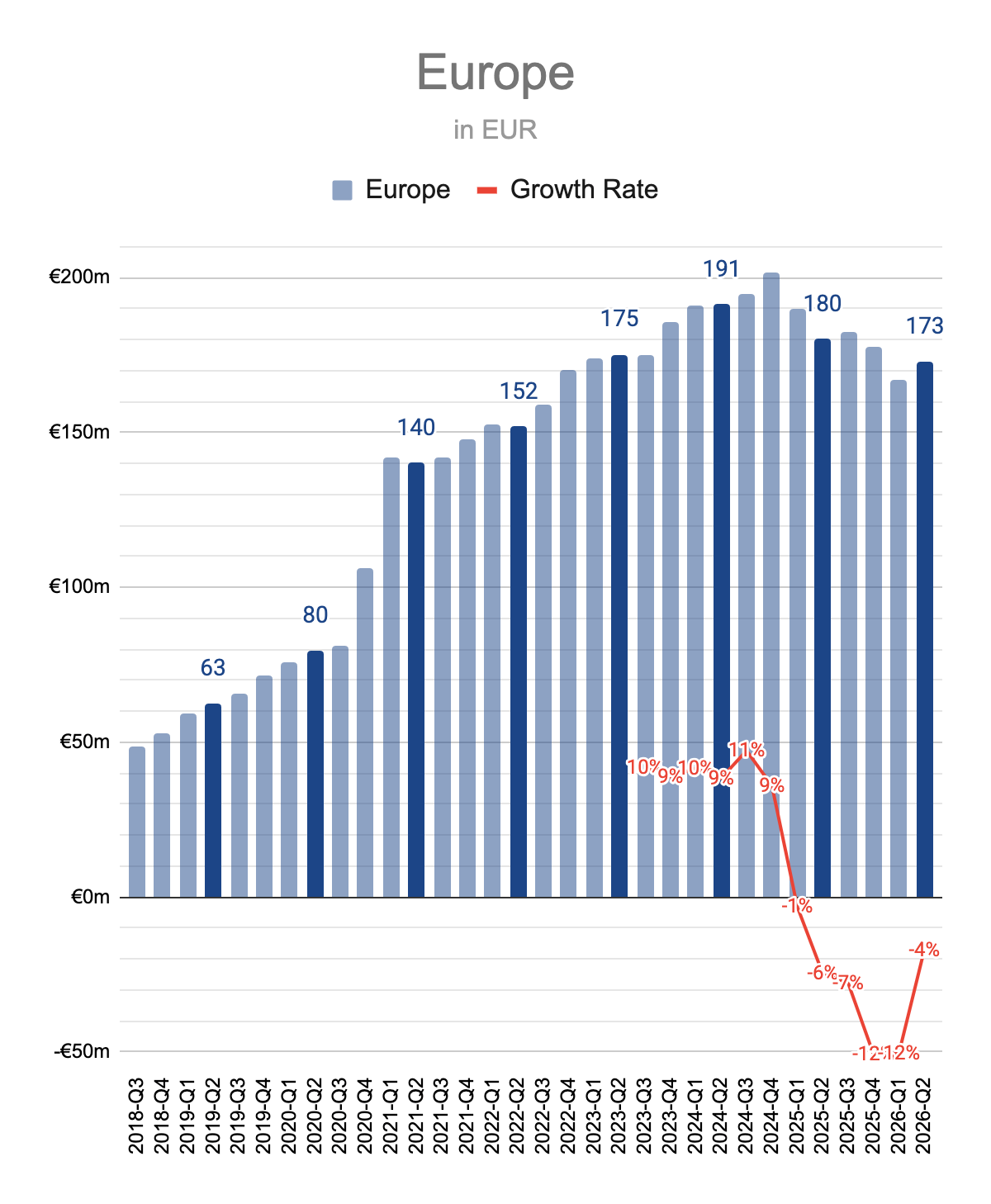

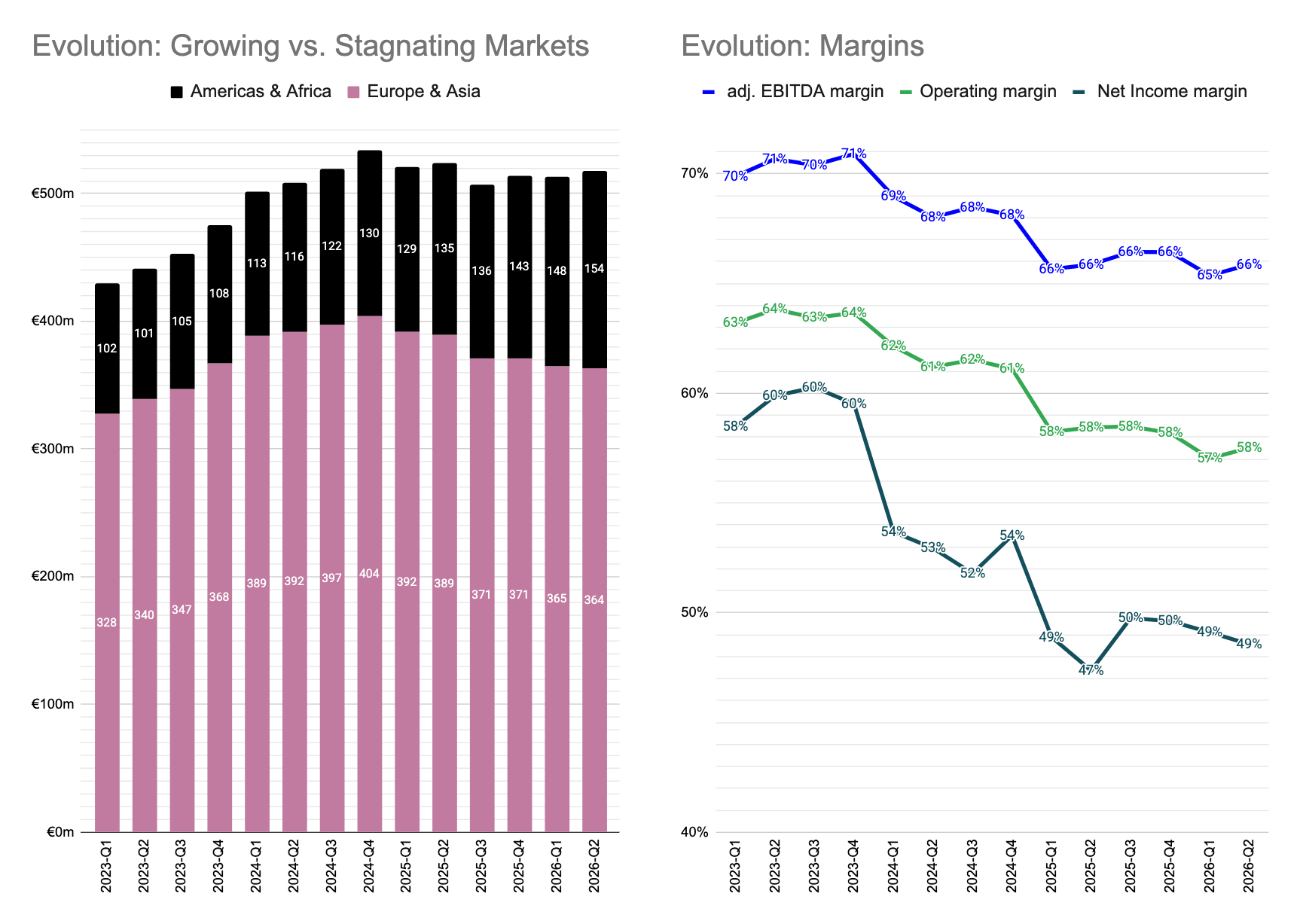

Europe

Management seems as surprised as anybody else that the decline in Europe has stabilized this quarter. Comments revolved around that player channelization into licensed casinos are “very weak”, raised taxes are not helping, the overall Live revenue decline was “mostly related to Europe”, World Cup did not provide a measurable boost and the future is unknowable.

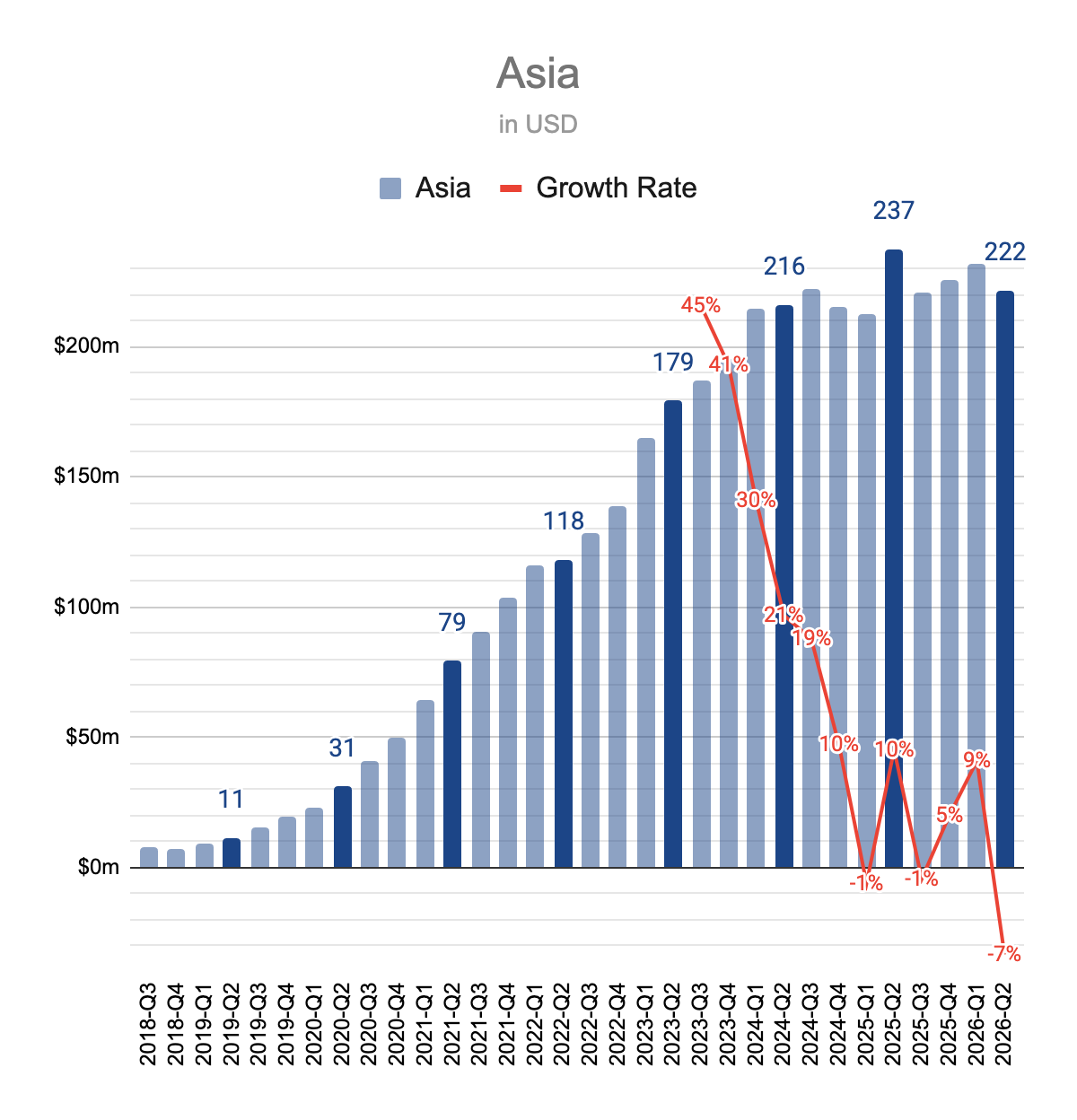

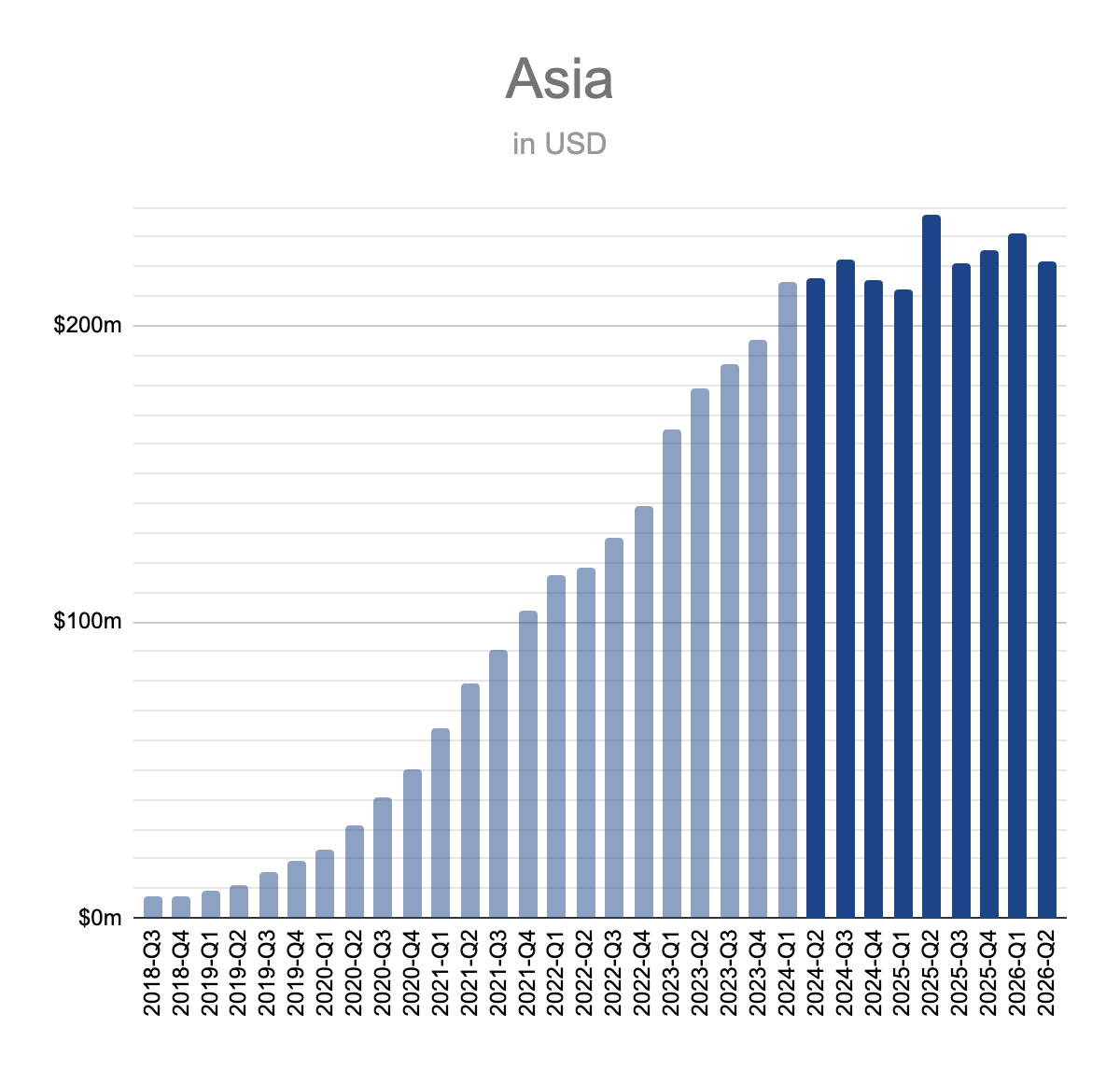

Asia

According to management, Evolution “took a step back” in Asia in the quarter.

The bigger issue seems to be that Evolution has generated no meaningful growth in Asia compared to 2 years ago. Especially for an iGaming company, this is a very long stretch of inertia to be described as temporary anymore.

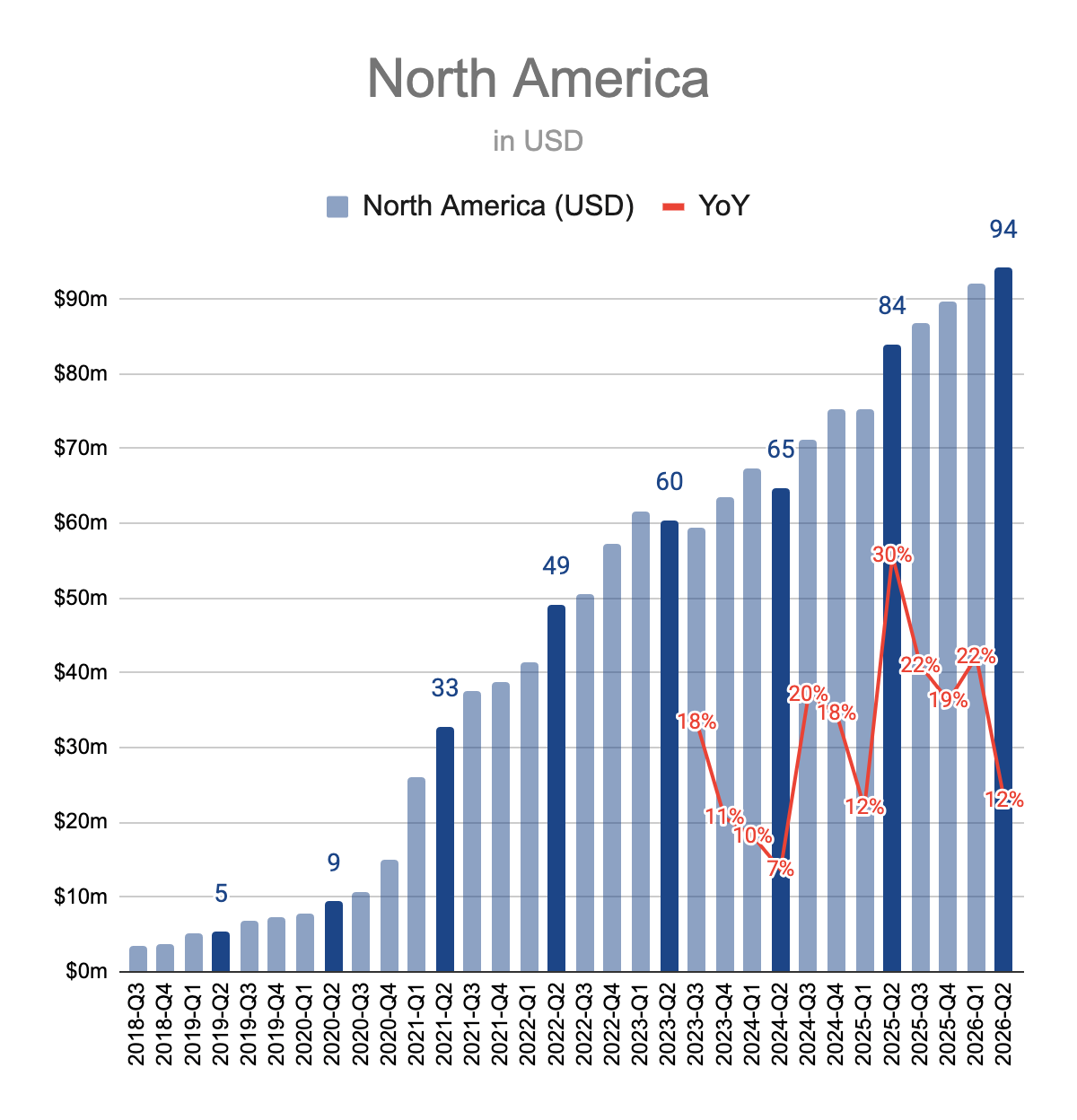

North America

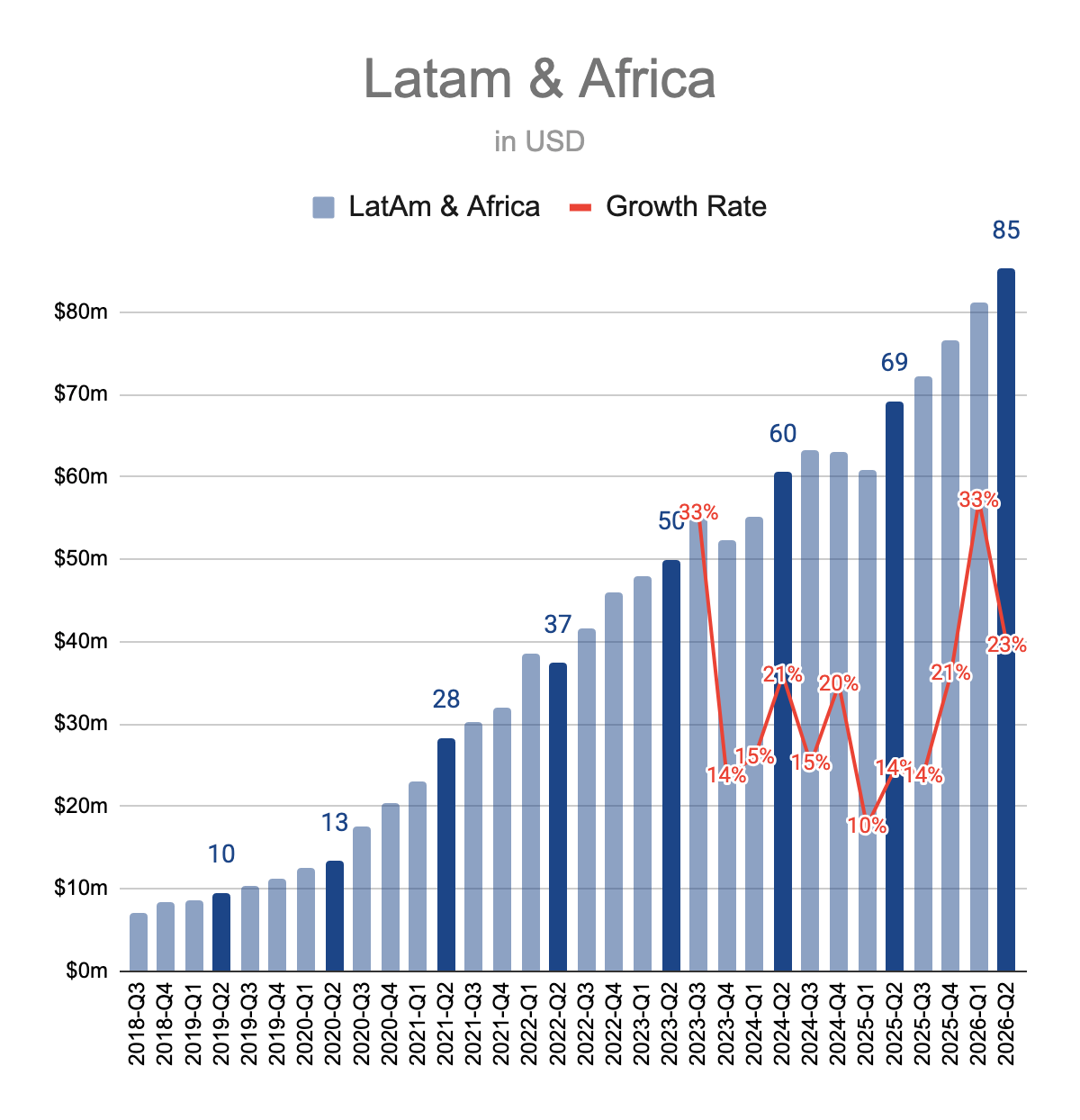

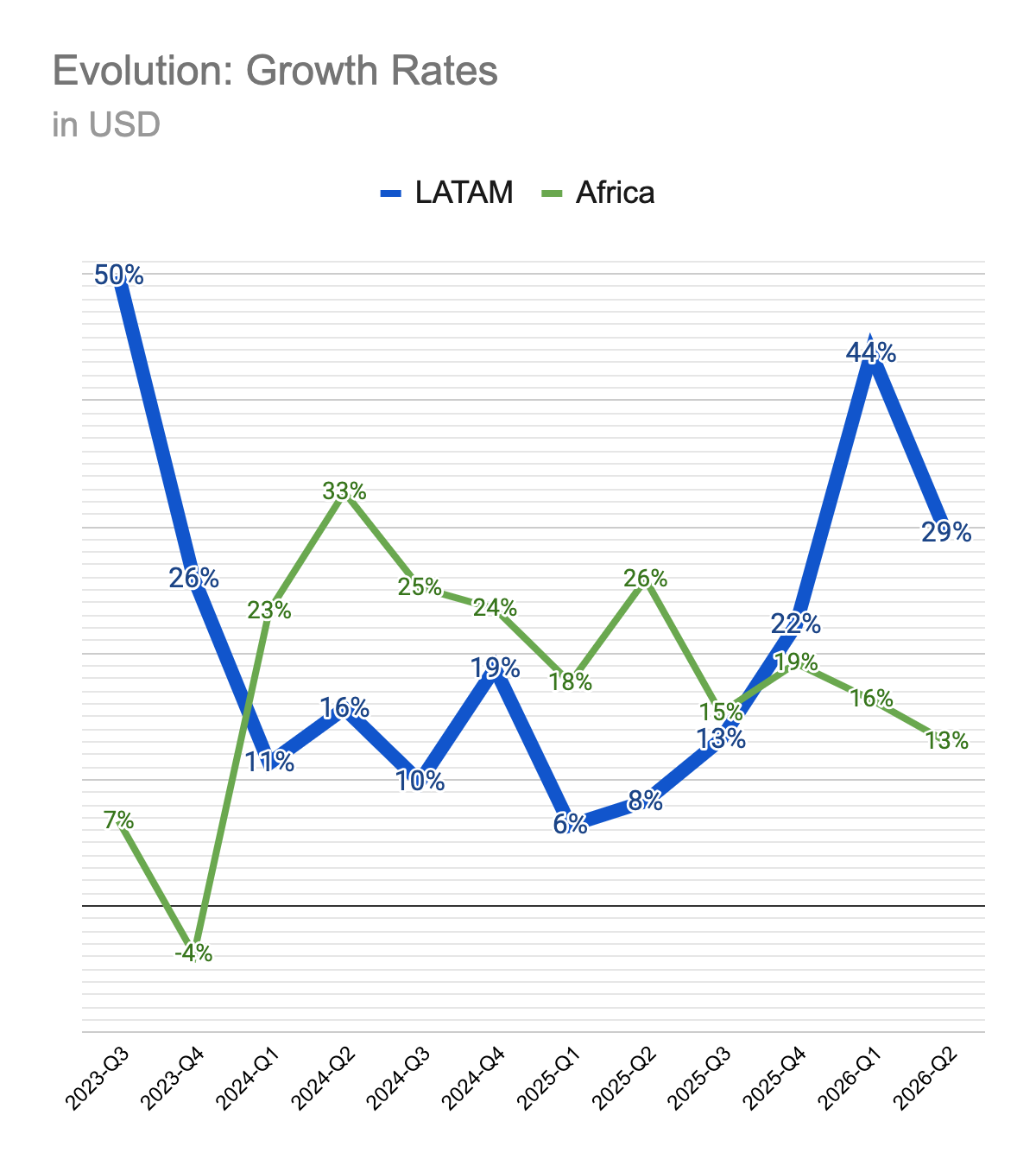

Latam & Africa

What may happen:

Growth in Americas and Africa

Company not only boasts — justifiably — about its potential in the growing markets in North and Latin Americas as well as Africa, but the results above and the studio build-out back this outlook.

Stagnation in Europe and Asia

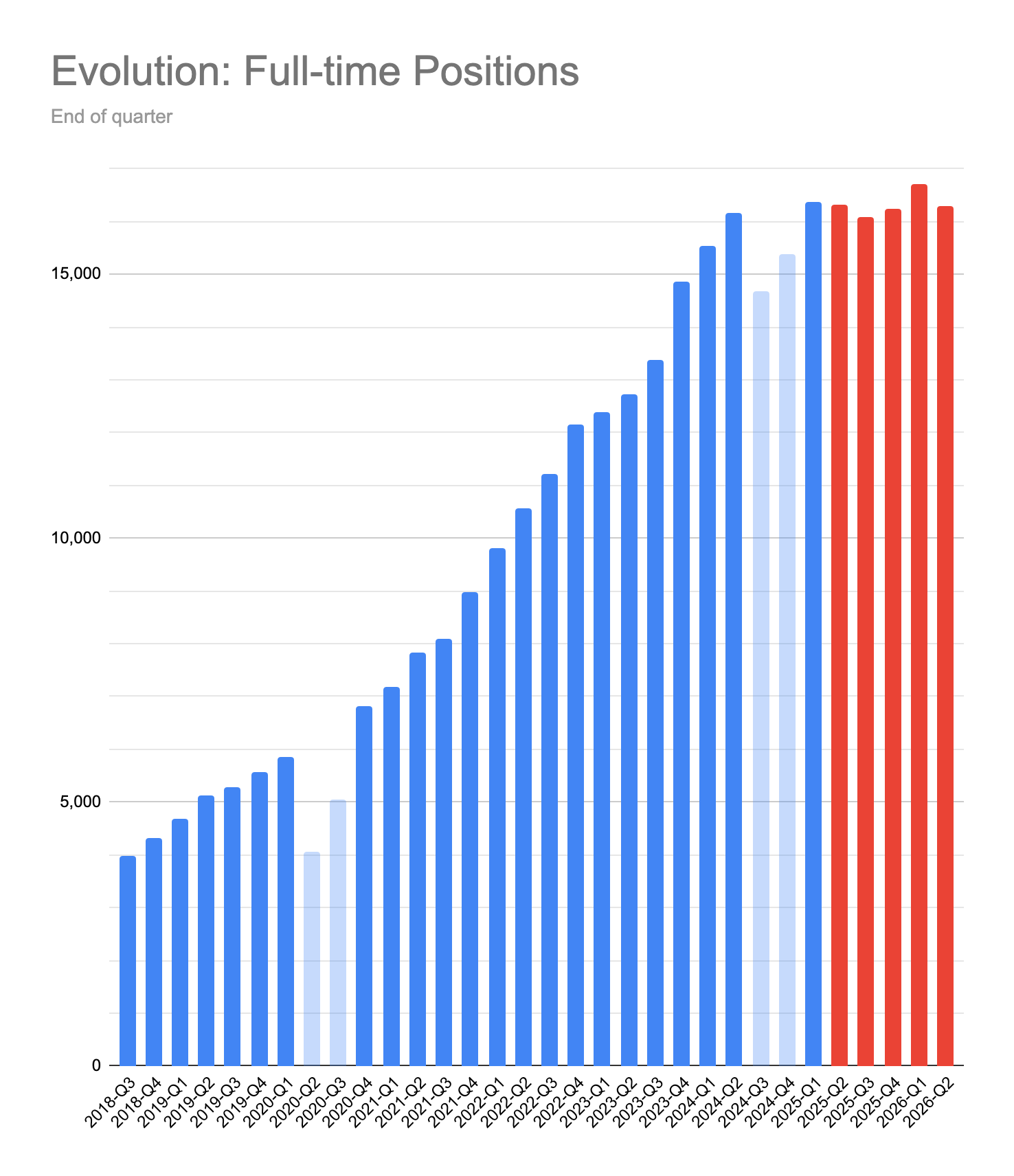

Over the last 5 quarters, Evolution’s overall employment level has stayed neutral.

However, the company has expanded its studio capacity greatly in the United States and Latin America in the mean time. This hints that the management has been downsizing its core network of studios in Eastern and Southern Europe that mainly serve Europe and Asia.

More than any comments, I believe in tracking what management does to measure their actual business outlook. The conservatism in managing the company’s core network capacity tells more about the immediate outlook in Europe and Asia than any commentary can.

Limits of Live

Evolution released Ice Fishing in August 2025. Since then, the game show has became a run-away hit and is regularly replacing the company’s long-time bestseller Crazy Time as the most popular game show in the world. However, throughout this rise to success, Evolution’s overall Live Casino sales have remained stagnant. This lack of growth despite introducing a new big hit could point to a couple of possible scenarios:

A) As the category leaders, Evolution’s game shows could be attracting a limited and not growing pool of potential players. Therefore, new games can, at best, cannibalize the player base from other Evolution games.

B) Evolution could be retreating in sales of its traditional table games where it is easier for the large and medium sized competitors to succeed in a relatively commodity product category without IP protections.

Margins under pressure

The shift from core networks serving Europe and Asia to the more fragmented markets of Americas continue to pressure the company’s operating leverage.

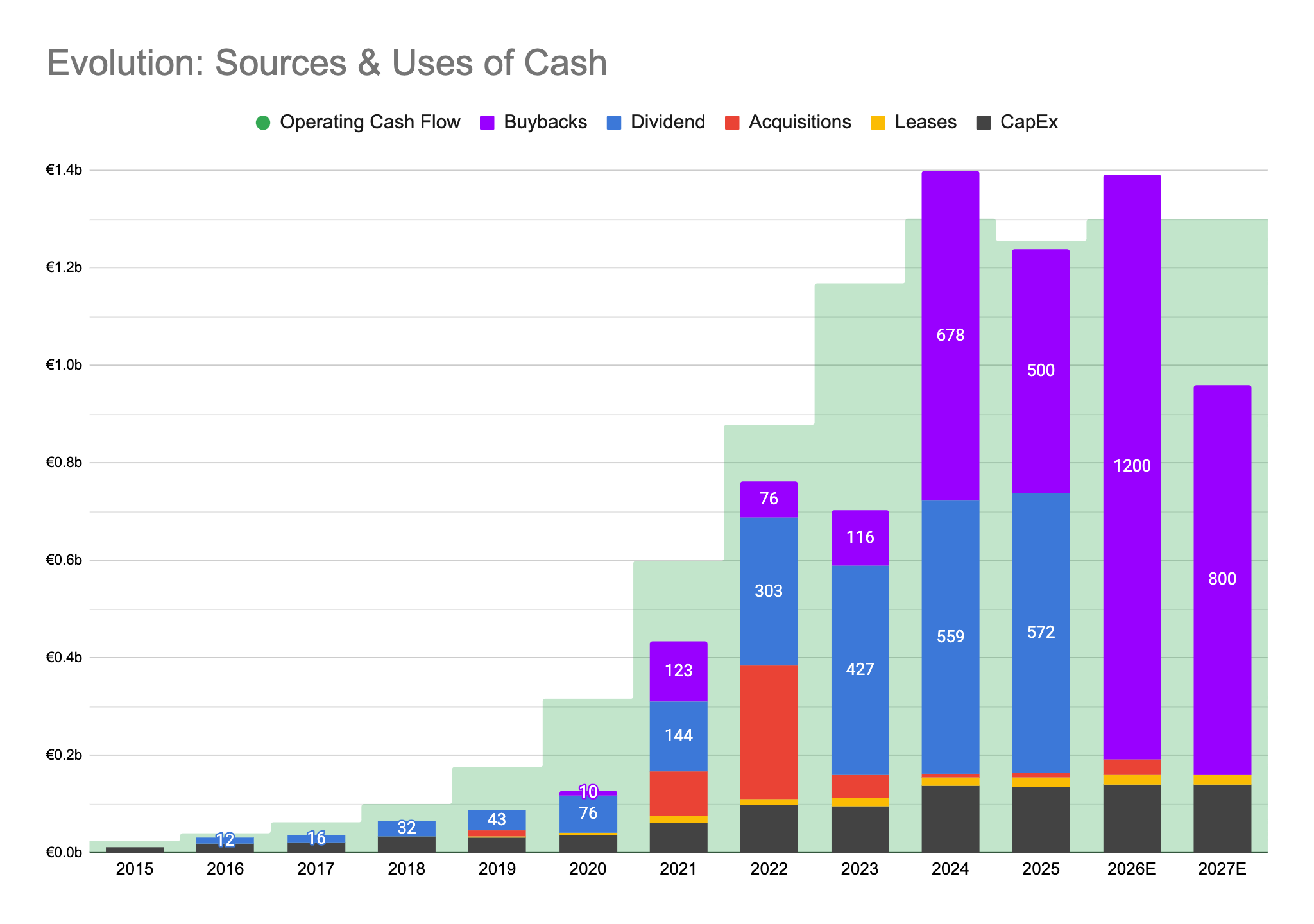

Buybacks into 2027

After a lengthy period of ambiguity, Evolution’s board finally decided to distribute almost all of 2025’s and 2026’s free cash flow as €2 billion of buybacks.

“We have kind of maxed out on what is possible. Its max is 25% of the daily volumes over the last 20 days’ daily volumes.” — CFO Andersson

Due to the trading limits, these buybacks can be expected to continue well into 2027.

Disclaimer: This is not investment advice. Please read the full disclaimer in the About page.